How to create a balance sheet: at a glance

A balance sheet lists everything your business owns (assets), everything it owes (liabilities), and what's left for owners (equity) at a specific point in time. To build one, gather your reconciled financial records, list and total your assets, list and total your liabilities, then calculate and verify the equation holds: assets = liabilities + equity. If both sides match, your balance sheet balances.

What is a balance sheet

A balance sheet shows all of your company's assets, liabilities, and equity at a given point in time. To make a balance sheet, compile your reconciled financial records; list and total your assets and liabilities; then compute and confirm that the following equation is true:

Assets = liabilities + shareholder’s equity

That's the balance sheet accounting equation, and it governs every transaction your business runs.

Your balance sheet statement is one of the three core financial statements every US business maintains alongside the profit and loss statement or income statement and the cash flow statement.

Your profit and loss statement shows whether you're making money over a period. Your cash flow statement shows how cash actually moved. A balance sheet for small businesses tells you whether you have enough working capital to cover the next 60 days, whether you're holding too much inventory relative to your payables, and whether your equity position is growing or eroding quarter over quarter.

What does a balance sheet look like

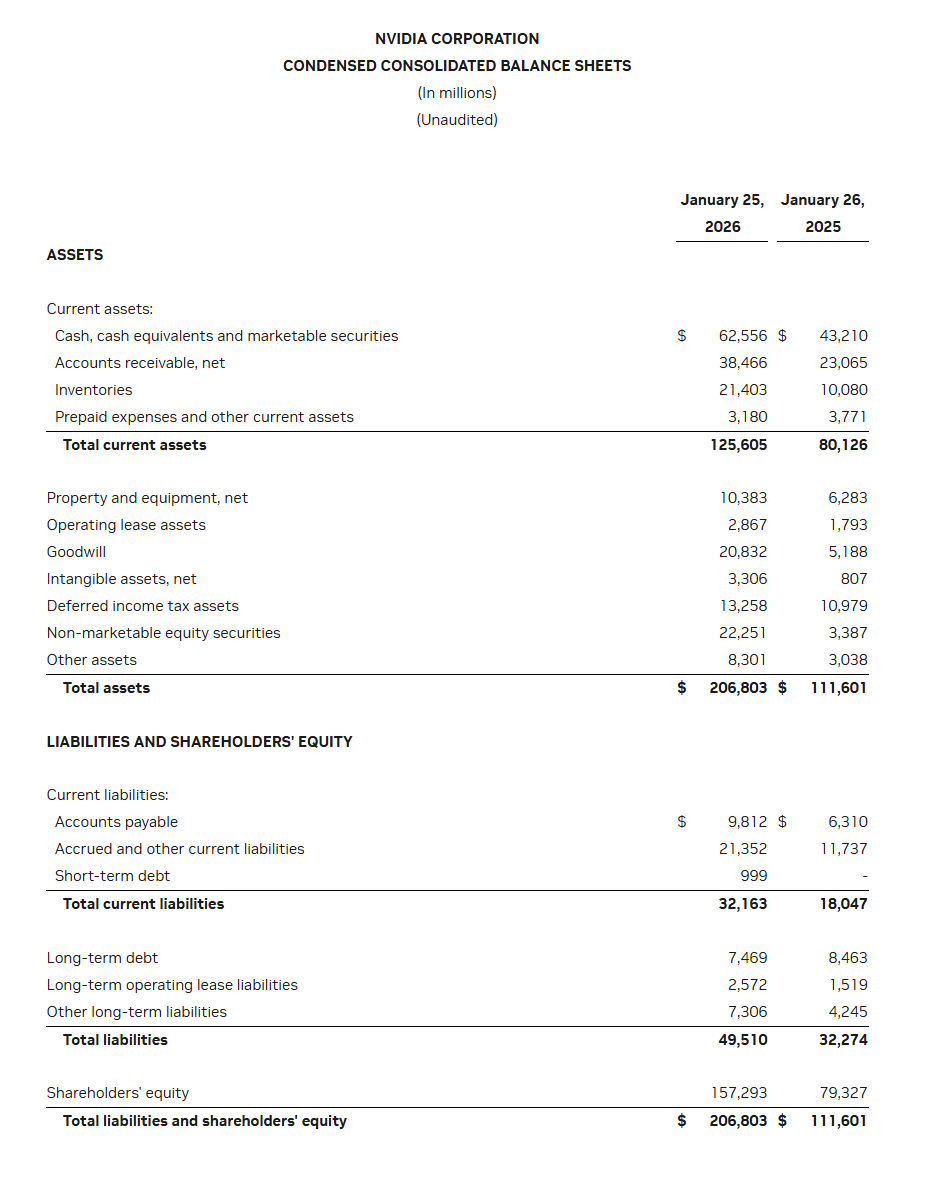

Let’s look at a real-world example: the Q4 FY26 balance sheet of Nvidia.

Source: NVIDIA

Understanding a balance sheet

To answer, 'What is on the balance sheet?' We need to understand the standard balance sheet layout. The items on a balance sheet are divided into three core pillars: assets, liabilities, and equity.

[Table:1]

1. Assets

Assets are everything your business owns or is owed that holds monetary value. Based on how rapidly each thing turns into cash, they are divided into two categories: current and non-current.

- Within a year, current assets become liquid. Prepaid costs, inventories, cash and cash equivalents, accounts receivable, and short-term investments are all included in this.

- Non-current assets take more than a year to convert to cash. Think real estate, machinery, automobiles and intangibles like trademarks and patents

Founder’s insight: Fixed assets must be valued at book value (original cost less cumulative depreciation) according to US GAAP. Tax laws operate in a different way. Instead of being depreciated over time, qualified equipment may be fully expensed in the year of purchase under Section 179. Your balance sheet figure and your tax deduction will differ as a result, and that's fine. Document it clearly and confirm the process with your CPA.

2. Liabilities

Liabilities are the debts that your company has to lenders, suppliers, workers, and tax authorities. They are separated by time horizon, much like assets.

- Current liabilities: Accounts payable, accrued costs, credit card balances, payroll obligations, deferred income, and the amount of any long-term loan that matures during the next year are all considered current liabilities and are due within a year.

- Long-term liabilities: Remaining loan amounts, SBA debt, prolonged lease commitments, and venture debt are examples of long-term liabilities that last longer than a year.

In founder-run companies, two categorization oversights frequently occur.

The first is loan splitting. The USD $12,000 that is due in the upcoming year on a USD $60,000 term loan falls under current obligations. Lenders will quickly notice if you put the entire money in one location since it misrepresents how much you owe in the near future.

The second is deferred revenue. When a customer pays USD $24,000 upfront for a two-year contract, it stays a liability on your balance sheet until the service is actually delivered.

[Table:2]

3. Shareholder’s Equity

In the balance sheet calculation, owner's equity is what remains after you subtract all liabilities from all assets. It represents the true ownership stake in the business.

It has three main components:

- Paid-in capital: Money invested by founders, shareholders, or from priced equity rounds.

- Retained earnings: Cumulative net income reinvested into the business — not paid out as distributions.

- Distributions or drawings: Amounts taken out by owners. These reduce equity.

Note: If equity is negative, your liabilities exceed your assets. This isn't always a crisis, but it does mean your liabilities exceed your assets, and you need to understand why and have a plan.

Why your business needs a balance sheet

A balance sheet provides a clear picture of your company's financial situation to investors, lenders, and your own finance team.

You create a balance sheet not only because it is necessary but also because all significant financial decisions, including capital raising, credit applications, and growth planning, depend on precise, organized data.

- Lender confidence: Before granting credit, banks and lenders check your solvency, debt-to-equity ratio, and current ratio.

- Investor clarity: Early-stage investors are interested in learning about your books, particularly the classification of convertible notes and SAFEs.

- Operational visibility: If you run a small business, a balance sheet helps you identify warning indicators before they become cash flow crises.

- Compliance and tax readiness: Accurate balance sheets are necessary for IRS reporting, state filings, and year-end tax preparation for US firms.

Founder’s insight: Prepare your balance sheet at minimum quarterly; go for monthly if your business carries debt, manages vendors, or has employees on payroll. Monthly tracking keeps you ahead of cash flow problems instead of discovering them too late to act.

How to build a balance sheet (step-by-step)

Learning how to make a balance sheet does not have to be complicated. Whether you are pitching investors or checking your cash flow, knowing how to prepare a balance sheet is a straightforward process when you break it down step-by-step.

Step 1: Reconcile first, build second

A balance sheet setup is always tied to a specific date (typically the last day of a month, quarter, or fiscal year). Pick your date first. Everything else flows from it.

Before you start listing numbers, pull these documents and reconcile them to your reporting date:

- Bank and credit card statements

- Accounts receivable aging report

- Accounts payable aging report

- Loan statements showing current balances (including SAFE agreements, if applicable)

- Fixed asset list with original costs and accumulated depreciation

- Payroll liabilities as of the reporting date

- Prior period balance sheet

If any of these aren't reconciled to the same date, stop and fix that first. A balance sheet built on unreconciled data will produce a number that looks complete but isn't reliable. That's worse than having no balance sheet at all, because you'll make decisions based on it.

Step 2: Build your assets section

Start with current assets. Work through each category systematically, assign USD values, and classify each item as current or non-current.

A few rules that matter:

- Use book value for fixed assets. Book value = original purchase cost - accumulated depreciation. List gross assets and accumulated depreciation as separate line items so anyone reading the sheet can verify the math.

- Apply an allowance for doubtful accounts. If some receivables are unlikely to be collected, reduce your A/R balance accordingly. Overstating receivables overstates assets.

- Don't include assets you no longer own. Even if they're still in your accounting software, clean your records first.

- Prepaid expenses are assets. Annual SaaS contracts, prepaid insurance, and similar items represent future economic value. List them.

Total your current assets, then your non-current assets separately. Here's how to find total assets on a balance sheet: total assets = current assets + non-current assets

Step 3: list and total your liabilities

List every financial obligation as of the reporting date, assign accurate USD values, and classify as current (due within 12 months) or long-term (due beyond 12 months).

Pay close attention to:

- Outstanding vendor invoices (accounts payable)

- Credit card balances

- Payroll taxes owed but not yet remitted

- Current portion of installment loans (split carefully from long-term balance)

- Deferred revenue

- SAFEs (if applicable)

- Venture debt (if applicable)

Total current liabilities and long-term liabilities separately, then combine for your total liabilities figure: total liabilities = current liabilities + long-term liabilities

Step 4: Calculate shareholder’s equity

In the balance sheet calculation, once you have total assets and total liabilities, equity is straightforward:

Shareholder’s equity = total assets − total liabilities

List the components individually: paid-in capital, retained earnings, and any distributions. Add them up. That total must equal the difference between your assets and liabilities.

Note: If preparing mid-year: Retained Earnings = Prior year-end RE + Current YTD net income (from profit and loss statement) − Distributions taken.

Step 5: Know how to balance a balance sheet when it doesn’t

At this step, the total assets must equal total liabilities plus total equity.

If the balance sheet statement doesn’t balance, the mismatch is telling you something specific. The most common causes and how to find them:

[Table:3]

How Aspire keeps your balance sheet accurate in real time

The hardest part of building a simple balance sheet for a small business isn't the math, and it's not how to generate a balance sheet either. It's having clean, categorized, up-to-date financial data to work from.

Most US founders rely on one or more of these tools to manage balance sheet accounting:

[Table:4]

For most growth-stage US businesses, the right stack combines a spend management platform like Aspire with your accounting software, so data flows in automatically rather than being entered manually.

Aspire1 connects your corporate cards2, vendor payments, and expense submissions to your books in real time. Transactions are auto-categorized and matched before month-end close begins, eliminating the manual data entry that creates single-entry errors and misclassified liabilities.

For US businesses managing multi-currency vendor payments, distributed teams, or cross-border operations, that real-time sync matters even more. You don't want your balance sheet to tell a different story in USD than your actual committed spend does in the underlying currencies.

When your financial operations run through one system, control compounds. You make faster decisions, catch problems earlier, and show up to lender and investor conversations with numbers you actually trust.

FAQs

What is the difference between a balance sheet and a profit and loss statement?

Understanding the profit and loss statement balance sheet relationship is essential. A profit and loss statement (also called a P&L statement or income statement) shows revenue, expenses, and net income over a defined period like a month, quarter, or year. A balance sheet shows financial position at one specific date. You need both to understand whether your business is profitable and whether it's solvent.

Is profit and loss the same as an income statement?

Yes. "Profit and loss statement" and "income statement" refer to the same document. Both report revenues, costs, and net profit or loss over a period. The term 'P&L statement' is more common among founders and small business owners; 'income statement' is the formal term used in US GAAP financial reporting. Either way, the numbers are the same.

What goes on a balance sheet?

A balance sheet includes three sections: assets (cash, receivables, inventory, prepaid expenses, net fixed assets), liabilities (accounts payable, accrued expenses, loans, deferred revenue, and any venture debt split by maturity), and owner's equity (paid-in capital and retained earnings). Current and non-current items are listed separately within assets and liabilities to allow liquidity analysis.

How do you balance a balance sheet?

A balance sheet balances when Total Assets equals Total Liabilities plus Total Equity. If it doesn't, the most common causes are unrecorded payables, single-entry transactions, depreciation miscalculations, or incorrect classification of instruments like SAFEs or loan principal. Use the diagnostic table in this guide to pinpoint the specific issue, each imbalance pattern has a distinct root cause.

What does a good balance sheet look like?

A healthy balance sheet typically shows a current ratio above 1.5, a debt-to-equity ratio under 2.0, positive and growing owner's equity, and fixed assets presented with gross cost and accumulated depreciation as separate lines. Retained earnings growing over time indicates profitability being reinvested into the business. Remember, benchmarks vary by stage and industry; compare against peers, not a universal standard.

Where do SAFEs go on a balance sheet?

It depends on the specific terms of the SAFE agreement and how your CPA interprets them under US GAAP. Many practitioners and VCs expect to see SAFEs in the equity section, since they have no interest rate or maturity date. However, some SAFE agreements contain cash-repayment provisions that can support liability treatment. Get this classification right before your next fundraiser.

What are the three financial statements and how do they relate?

The three core financial statements are the balance sheet, the profit and loss statement (income statement), and the cash flow statement. Net income from the P&L feeds into retained earnings on the balance sheet. The cash flow statement reconciles net income with actual cash movement and explains changes in the balance sheet's cash line. Together, they give a complete picture of financial health.