Can expenses be liabilities

No, expenses and liabilities are not the same.

An expense is the cost of running your business. It appears on your income statement, reducing your net profit. A liability is a financial commitment you have to a third party. It is recorded on your balance sheet and reflects a future cash outflow.

In a nutshell, expenses track how much you've previously spent. Liabilities represent what you still owe.

Types of expenses

An expense is any cost tied to running your business day to day.

When you pay your team, renew a SaaS subscription, or cover a month of office rent, those are expenses. Regardless of when cash actually moves, expenses reduce your net income in the period they incur.

Expenses live on the income statement (your P&L). They do not go on the balance sheet. If someone asks whether expenses are liabilities or assets, the answer is neither. Expenses reduce equity by lowering retained earnings over time.

The IRS allows most ordinary and necessary business expenses to be deducted in the year they’re incurred. If you classify costs correctly, you lower your taxable income immediately. That's a real cash impact, not just accounting.

Different kinds of expenses

- Fixed expenses stay constant regardless of business performance. For example, rent, salaries, and insurance premiums don't change month to month. They create a predictable cost floor that makes budgeting straightforward but also sets a baseline burn you can't easily reduce in a slow month.

- Variable expenses scale with your activity. AWS hosting costs, contractor fees, and shipping are all examples that grow as output grows — which means they can spike faster than revenue catches up during a high-growth period.

Understanding the fixed and variable cost difference comes down to one question: does this cost change when your revenue does? Fixed costs don't. Variable costs do. Knowing which is which tells you exactly where your burn is controllable and where it isn't.

- Operating expenses (OpEx) are the costs directly tied to running the core business day-to-day, like payroll, software subscriptions, marketing spend, and utilities.

- Selling, general, and administrative (SG&A) expenses cover the cost of selling your product and running the business infrastructure. Some of the examples of SG&A expenses are sales commissions, executive salaries, legal fees, and office costs. Investors closely monitor SG&A because an increase in SG&A as a percentage of revenue indicates that overhead is growing faster than the business.

- Non-operating expenses sit outside the core business. Interest payments on a business loan, inventory write-offs, and losses from asset sales are the most common examples.

- Cost of goods sold (COGS) captures only the direct costs tied to what you produce or sell, like raw materials, shipping, storage costs, and production labor. Keeping COGS and OpEx separate is non-negotiable for accurate gross margin reporting.

Expenses examples

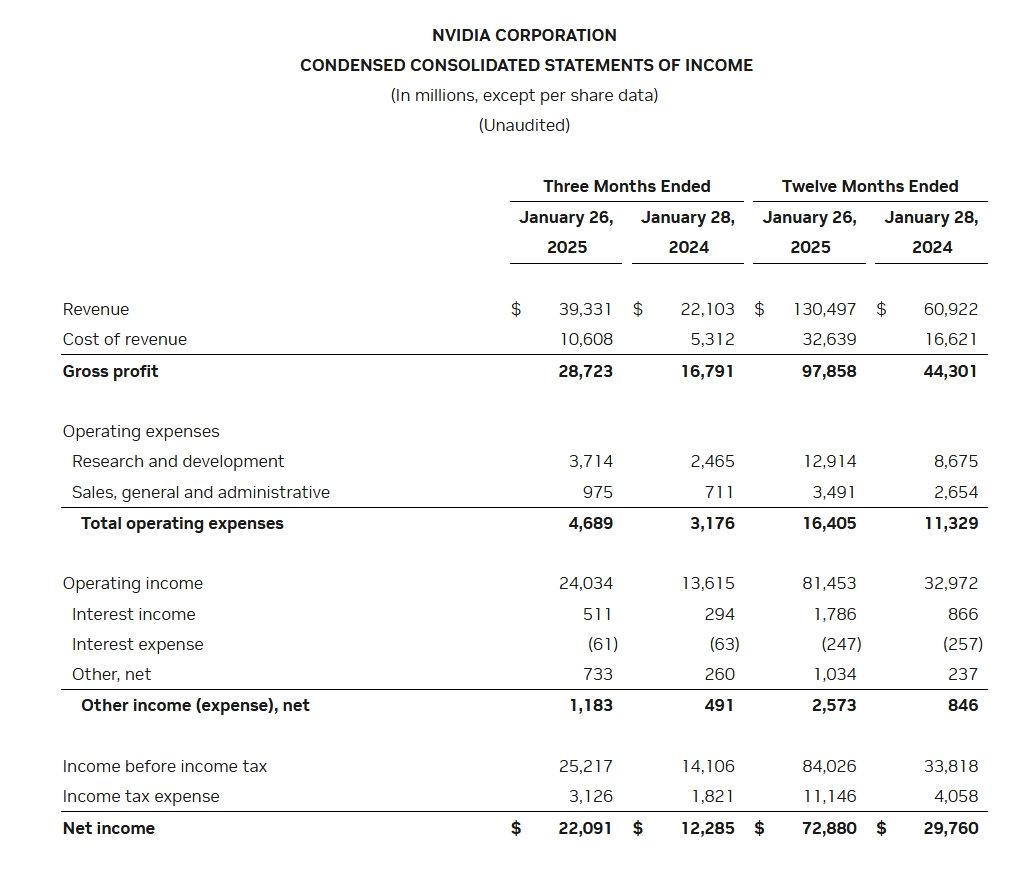

Here’s a real example from NVIDIA’s fourth quarter fiscal 2025 income statement. The income statement directly shows expenses because they decrease profit in the period they occur.

Definition of a liability

A liability is money your business owes but hasn’t paid yet.

That includes loans, unpaid invoices, and upcoming payroll. If the cash hasn’t left your account, but the obligation exists, it’s a liability.

This is why it is included on the balance sheet. It shows what’s going out next, not what has already been spent.

Not all liabilities are a problem. Often, they show momentum. Venture debt, a working capital line, or prepaid annual contracts all appear as liabilities. They often mean you’re investing in growth or getting paid upfront.

Types of liabilities

Current liabilities: Liabilities that are due within a year are known as current liabilities. This includes outstanding taxes, short-term loans, accrued salaries, and accounts payable.

Your current ratio, which is determined by dividing current assets by current obligations, is one of the first factors a lender considers before extending credit, as current assets are typically used to pay debts.

Non-current liabilities: These are debts that have been outstanding for more than a year. This category includes long-term leases, equipment finance, and business loans.

They don't put you under immediate financial strain, but they do have an impact on your long-term solvency and your debt-to-equity ratio, which investors use to gauge how indebted your company is.

Contingent liabilities: Potential obligations connected to a future occurrence that could or might not happen are known as contingent liabilities.

Common examples are an ongoing legal action or an unsettled warranty claim. When the result is likely and the amount can be fairly approximated, you are obliged by US GAAP to record a contingent obligation on the balance sheet.

Note: Deferred revenue is one that many SaaS teams find confusing. If a customer pays USD $12,000 upfront for an annual contract, that money is not revenue yet. Until you deliver the service each month, it sits as a liability.

Example of Liabilities

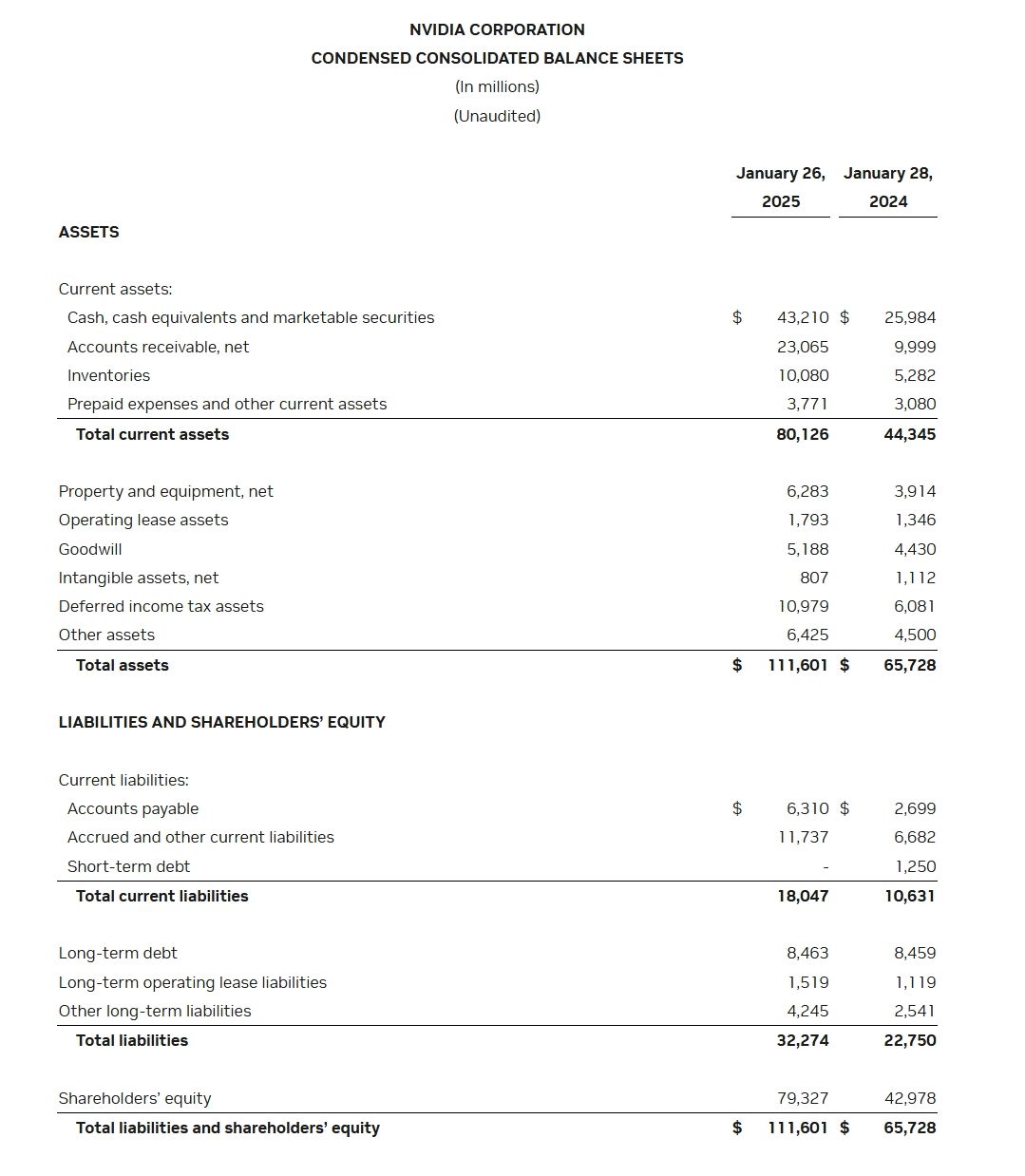

Take NVIDIA’s Q4 fiscal 2025 balance sheet. You can see the current and non-current liabilities are listed under the liabilities and shareholders’ equity section.

Liabilities vs expenses: what is the difference between a liability and an expense

The difference between expenses and liabilities comes down to where they appear in your financials and how they impact profit and obligations.

[Table:1]

The liabilities vs expenses dilemma: when an expense also becomes a liability

This is where the liabilities vs. expenses difference overlaps and where most teams get it wrong.

It comes down to timing. Specifically, how your accounting method records costs.

Under accrual accounting, you record a cost when it’s incurred, not when you pay it. That creates a window where the same transaction shows up in two places. It is recorded as an expense on your P&L and as a liability on your balance sheet.

For example, you receive a $5,000 legal invoice in December but plan to pay it in January.

In December, the cost is already real. You record a $5,000 expense, which reduces your profit. At the same time, you record $5,000 in accounts payable because you still owe that amount.

In January, when you pay the invoice, cash goes out and the liability is cleared. Nothing new hits your expenses, because that cost was already recognized.

If you were using cash accounting, this would look different. The entire transaction would only show up when the payment is made. No expense, no liability until cash moves. Which means your books can miss short-term obligations entirely.

That’s the core difference.

Accrual accounting shows both what you’ve spent and what you still owe. Cash accounting only shows what has already moved through your bank account.

The takeaway: Under accrual accounting, an unpaid expense becomes a liability until it’s paid. One transaction, two entries.

Expense vs liability account: impact on your financial statements

Expenses and liabilities show up in different places and affect your numbers in different ways.

Income statement (P&L)

Expenses reduce net income in the period they’re incurred. Higher expenses lower margins and increase burn, directly affecting EBITDA.

Balance sheet

Liabilities reflect what you owe. If liabilities increase without a matching increase in assets, equity decreases. Ratios like the current ratio and the debt-to-equity ratio depend on accurate liability classification.

Founder’s insight: Your P&L can look healthy while your balance sheet is under serious pressure. With 82% of small business failures linked to cash flow problems, the gap between what you've spent and what you still owe is the most common financial blind spot in early-stage businesses.

How to record liabilities and expenses

Every transaction has two sides: a debit and a credit. Getting the classification right at the point of entry is what keeps your books clean downstream.

Recording an expense

You record an expense when the cost is incurred.

If you pay for it immediately, you debit the expense account and credit cash. If you haven’t paid yet, you credit accounts payable instead.

For example, if you pay $3,000 in monthly payroll, you debit the salaries expense by $3,000 and credit cash by $3,000.

The cost is now reflected in your income statement, and your cash balance is reduced.

Recording a liability

Credit the liability account when the obligation is created (increases what you owe). Debit the corresponding asset or expense account.

For instance, you instantly record a $3,000 vendor invoice that is due in 30 days. You credit accounts payable with $3,000 and debit the expense account with $3,000. This entry records the amount you owe as well as the cost.

When you pay the invoice, $3,000 is debited from accounts payable and $3,000 is credited to cash. Nothing new is noted as an expense, and the liability has been settled.

Manual inputs frequently result in missing liabilities or incorrectly categorized expenses, which may affect your financial statements.

With roughly 61% of small business owners unable to track monthly income and expenses in real time, the risk isn't just theoretical.

Aspire's direct integrations with QuickBooks and Xero auto-map every corporate card transaction to the correct ledger category at the point of spend, cutting manual entry errors before they reach your books.

Liabilities vs expenses: why proper classification matters

Proper classification has direct consequences on three things that determine whether your business can grow.

Tax accuracy

The IRS allows you to deduct business expenses. If you misclassify a loan repayment as an operating expense, you're claiming a deduction you're not entitled to, and it comes with penalties.

Conversely, misclassifying an expense as a liability means you're not taking a deduction you've earned, which inflates your taxable income unnecessarily.

Fundraising and valuation

Investors calculate your debt-to-equity ratio directly from your balance sheet. If liabilities are buried inside expense lines, your margins look artificially worse and your actual debt load is invisible.

Creditworthiness

Banks look at total liabilities and your current ratio before approving a line of credit or business loan. If debt is hidden as expenses or expenses are hidden as liabilities, the lender is reading a distorted picture, which can lead to loan applications being declined.

Best practices for managing liabilities and expenses

Classification decisions mostly happen at the transaction level.

Use a consistent expense categories list

Map every transaction to a predefined category at the point of entry. Inconsistent categorization is the primary driver of misclassification.

Reconcile corporate card spend regularly

Credit card reconciliation, or matching card statements to your general ledger, catches miscategorized transactions before they compound. The fastest way to reconcile corporate card expenses at month-end is to ensure every transaction is coded correctly at the time of the swipe.

Aspire corporate card2 and expense management tools give your finance team real-time visibility of spending as it happens and track company expenses. Every transaction is categorized automatically, synced to your accounting stack, and available for reconciliation without manual intervention.

Read your balance sheet monthly, not just your P&L

Your income statement shows profitability. Your balance sheet shows solvency.

A business with strong revenue and a growing stack of unpaid liabilities is not a healthy business; the P&L just makes it look like one.

The bottom line

Your income statement tells you whether the business is profitable. Your balance sheet tells you whether it's solvent. Neither statement is useful if liabilities are misclassified as expenses or expenses are recorded as liabilities.

When your books accurately separate what you've spent from what you still owe, your tax position is defensible, and your investor conversations are grounded in real numbers.