Routing number vs account number: key differences

The easiest way to understand the difference between routing numbers and account numbers is to compare them directly.

[Table:1]

The key difference: routing numbers are shared across many customers at the same bank, while account numbers are unique to you. Both are required for electronic payments to work.

Given above is a quick sample to help you find these numbers.

What is a routing number on check?

A routing number is a 9-digit code that identifies your bank or credit union within the US banking system. It tells the financial network which institution holds your account so payments can be routed to the correct bank.

You can think of it in terms of a bank's address. When you make a payment using an ACH transfer or a wire transfer, the routing number is essentially sending that payment to the proper financial institution. And then within that financial institution, the account number is sending that payment to the proper account.

Where to find your routing number on check

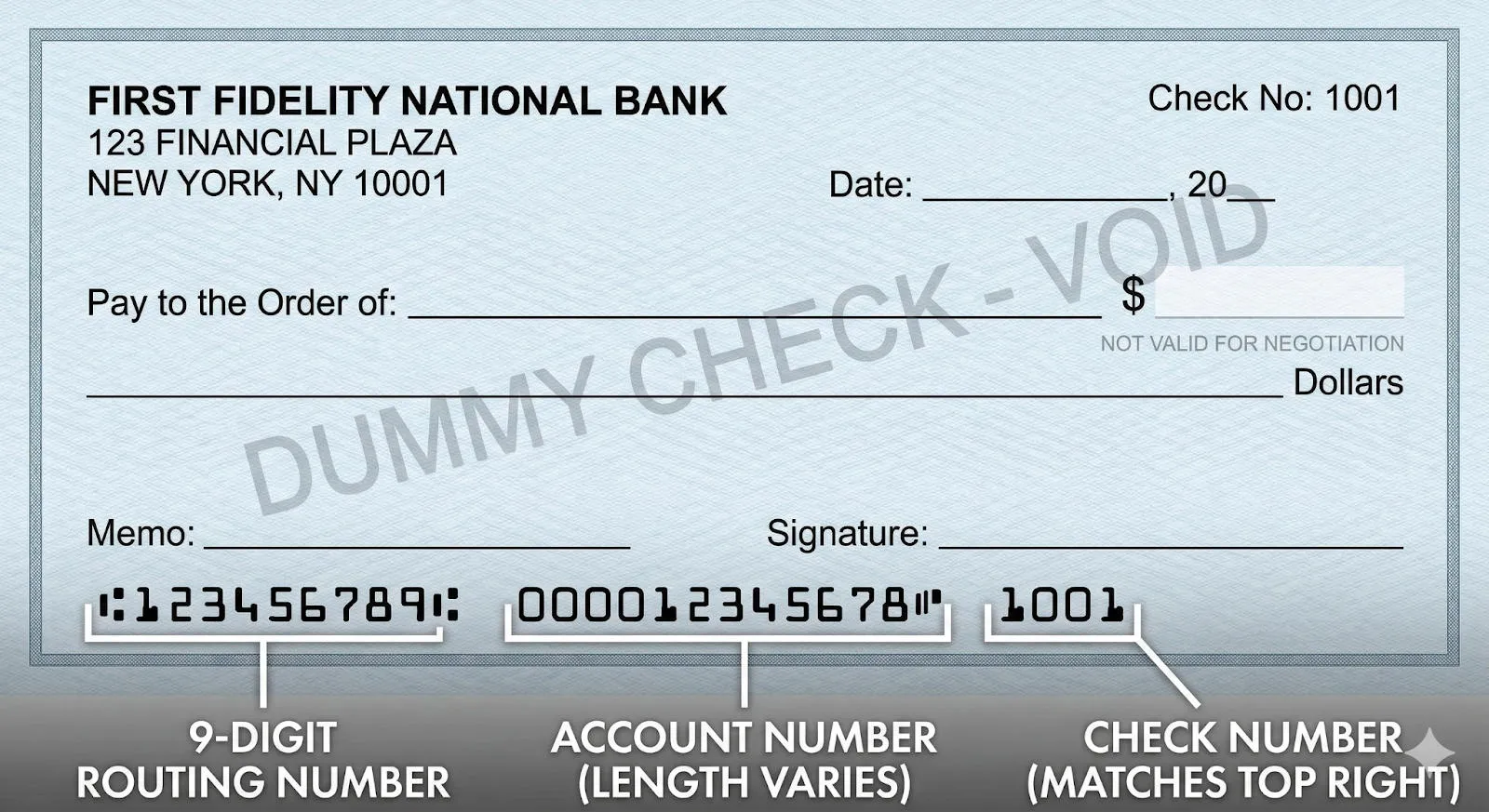

The easiest place to find your routing number is on a check. It's the first 9-digit number on the bottom left, before your account number.

You can also find it by:

- Logging into your online banking portal (usually under account details)

- Opening your bank's mobile app (typically in account settings)

- Checking your monthly bank statement (often listed at the top)

- Calling your bank directly

- Searching your bank's website (most banks publish routing numbers publicly)

What routing numbers identify

Routing numbers identify:

- Your bank or credit union within the US banking system

- Which financial institution holds your account

- Where payments should be routed before reaching your specific account

Why routing numbers matter in banking.

Routing numbers handle the first step in any electronic payment: getting money to the right bank. Without the correct routing number, the payment can't reach your bank at all. It gets rejected before it even attempts to hit your account.

The US has over 4,000 banks and credit unions. The routing number is how the payment network distinguishes one institution from another and ensures funds arrive at the correct bank before the account number takes over to direct them to your specific account.

How many digits are in a routing number

Routing numbers are always exactly 9 digits. This format is standardized across all US banks and credit unions.

The first 4 digits identify the Federal Reserve routing symbol, which indicates the bank's location and Federal Reserve district. The next 4 digits identify the specific bank. The last digit is a checksum used to verify the routing number is valid.

This 9-digit format has been standard since 1910 when the American Bankers Association created the system to streamline check processing.

Understanding routing number format

The routing number has the following structure: XXXXYYYYC, where there are 9 digits in total.

The first 4 digits, XXXX, indicate the Federal Reserve Routing Symbol, which reveals the Federal Reserve District and Institution Type.

The first 2 digits of the routing number range between 01-12 for primary banks, 21-32 for thrift institutions such as credit unions, and 61-72 for electronic payment processors.

The next 4 digits, YYYY, indicate the financial institution, while the final digit, C, is the check digit, which reduces the possibility of misrouted funds due to typos and other numerical mistakes.

[Table:2]

Source - https://www.routingnumber.com/

For example, 111000038 belongs to the Federal Reserve Bank in Minneapolis. The check digit ensures the number is mathematically valid before processing any payment.

Most founders never need to understand this structure, but it explains why entering even one wrong digit causes payment failures.

Large banks often have multiple routing numbers depending on the state where you opened your account or the type of transaction. For example, Bank of America has different routing numbers for accounts opened in California versus New York. Wire transfer routing numbers can also differ from ACH routing numbers at some institutions.

What is an account number on check?

An account number on check is the unique identifier for your specific bank account. While a routing number points to your bank, the account number points to your individual account within that bank.

No two accounts at the same bank share the same account number. It's how the bank distinguishes your account from the thousands or millions of other accounts they manage.

Where to find your account number on check

Your account number appears on checks as the second set of numbers on the bottom, between the routing number and the check number.

Other places to find it:

- Online banking under account details

- Your bank's mobile app

- Monthly bank statements

- Deposit slips

- By calling your bank's customer service line

What account numbers identify

Account numbers identify:

- Your specific checking or savings account

- The account holder or business entity

- Where funds should be deposited or withdrawn from

If the routing number is the bank's address, the account number is your apartment number within that building. Both are required to complete a payment.

Why account numbers matter in banking

Account numbers ensure payments reach the correct account. Even if the routing number successfully directs a payment to the right bank, the account number determines whether the money lands in your account or someone else's.

Transposing even one digit in your account number can send payments to the wrong account or cause the transaction to fail entirely. Banks can reverse some mistakes, but it requires manual intervention and can delay payments by days or weeks.

How many digits are in a bank account number

Account numbers vary in length depending on the bank. Most range from 8 to 12 digits, though some banks use as few as 5 or as many as 17. There's no standard format across institutions.

When routing numbers and account numbers are used

Both numbers are required for most electronic payments, but the context varies.

Direct deposits

When you set up direct deposit for payroll or customer payments, you need to provide both your routing number and account number. Employers, clients, and payment platforms all use the same information: routing number first, account number second.

ACH transfers

ACH transfers require both numbers. Whether you're sending or receiving money via ACH, the routing number identifies the bank and the account number identifies the account. ACH is the most common form of electronic payment in the US. Payroll, vendor payments, subscription billing, and tax refunds all run through ACH networks.

Wire transfers

For domestic wire transfers, you will need to provide your routing number and account number. However, some banks have a different routing number for wire transfers than for ACH transactions, so be sure to check with your bank to determine the routing number to use.

For international wire transfers, routing numbers are often not necessary and SWIFT numbers or IBAN numbers will be used depending on the country.

Bill payments

When you set up automatic bill payments through your bank or a service provider, you provide your routing and account numbers. The payment processor uses these to debit your account on the scheduled date.

Here's when each number is required:

[Table:3]

Why banks use both routing numbers and account numbers

The dual-number system exists because the US banking network needs to route payments through thousands of financial institutions.

The routing number tells the network which bank to send the payment to. Without it, there's no way to know where the money goes. The US has over 4,000 banks and credit unions, and the routing number is how the system distinguishes one from another.

Once the payment reaches the correct bank, the account number directs it to your specific account. A single bank might have millions of accounts, so the account number ensures funds land in the right place.

This two-step system has been the foundation of US electronic payments since the early 1900s. It's why both numbers are required for nearly every transaction.

How to keep your routing and account numbers secure

Routing numbers aren't secret. Banks publish them on their websites. You can Google "Chase routing number" right now and find it in seconds.

Account numbers are different. That's the private half of the equation, and losing control of it creates real problems.

Don't share your account number publicly

This sounds obvious, but founders do it all the time. Posting a screenshot of a payment confirmation on social media. Sending account details in a Slack channel with contractors you barely know. Including banking info in a public Google Doc for "the team."

If it's online and accessible to people you don't personally trust, don't put your account number there.

Verify recipients before sharing

A vendor emails asking for updated banking details. Seems routine. Except the email address is slightly off, by one character different from their real domain. You send the info. Now someone you've never met has full access to pull money from your account.

Before you share account numbers, verify who's asking. Call them directly using a number you already have, not one from the email. If it's a new vendor, confirm their legitimacy through multiple channels.

Use secure channels

Regular email isn't encrypted. If you're sending account details through either, you're sending them in plain text across the internet.

Use your bank's secure messaging system. Use encrypted email if your recipient supports it. At minimum, split the information across two separate messages sent through different channels—routing number in one, account number in another.

Monitor your account regularly

Most fraud gets caught because someone notices a transaction that doesn't belong. Set up alerts for debits over a certain amount. Check your account every few days, not once a month when the statement arrives.

The faster you catch unauthorized activity, the easier it is to reverse.

Be cautious with ACH authorizations

When you share your routing number and account number with someone for the purpose of ACH, you're not simply giving them permission to make one transaction from your account. You're giving them the ability to take money from your account as many times as they wish, in whatever amounts they wish, until such time as you revoke that permission.

Don't share your routing number/account number with just anybody. The random contractor you hired through Upwork last week? Not so much.

Shred old checks and statements

Tearing a check in half and tossing it in the trash isn't enough. Your account number is still readable. Anyone with access to your garbage now has access to your banking details.

Shred checks, statements, and any documents with account numbers before you throw them away. Or burn them if you don't have a shredder.

If your account number gets compromised, contact your bank immediately. They can freeze the account, reverse fraudulent transactions if caught quickly enough, and issue a new account number. It's a hassle, but it's better than watching your balance drain while you're trying to figure out what happened.

Open a business account built for payments

Once you understand routing and account numbers, you need banking infrastructure that actually works for business operations. Aspire1 offers business accounts1 designed for founders managing vendor payments, payroll, and transfers without traditional banking friction.

Multi-currency support*, faster settlement times, and accounting integrations that sync automatically mean you spend less time on banking admin and more time running your business. Open an account in minutes and get the routing and account numbers you need to start processing payments immediately.

Open an Aspire account and simplify how you handle business payments.