.png)

Summary

- Prepare for fundraising early by extending your cash runway and maintaining at least 24–36 months of clear cash flow visibility

- Expect stricter term sheets in 2026 and review clauses beyond valuation, especially control rights, liquidation preferences, and future fundraising restrictions

- Set realistic valuations based on fundamentals to avoid down rounds and weaker negotiating power in later funding stages

- Invest in strong financial reporting, governance, and a clean data room to build investor confidence in a cautious market

- Decide upfront how much control you are willing to trade for capital, as growth funding increasingly comes with shared decision-making

For founders and CFOs in Singapore, the past few years have redefined what ‘normal’ looks like in venture capital. What began as a sharp correction in 2022 has evolved into a more disciplined, fundamentals-driven funding environment by 2026.

A tale of two realities, revisited

Between 2022 and 2025, global markets were shaped by overlapping disruptions:

- The aftershocks of COVID-19, prolonged geopolitical conflicts, elevated interest rates, crypto market failures, and repeated rounds of layoffs across global tech firms tightened liquidity worldwide.

- At the same time, rapid adoption of AI, automation, cloud infrastructure, and fintech platforms accelerated productivity gains, allowing leaner companies to scale faster with fewer resources.

Singapore sat at the intersection of these forces. While the city-state remained one of Asia’s most resilient startup hubs, venture capital became more selective rather than scarce. IPO activity across global tech markets stayed muted longer than expected, and later-stage funding, especially Series C and beyond, saw a meaningful reset rather than a collapse.

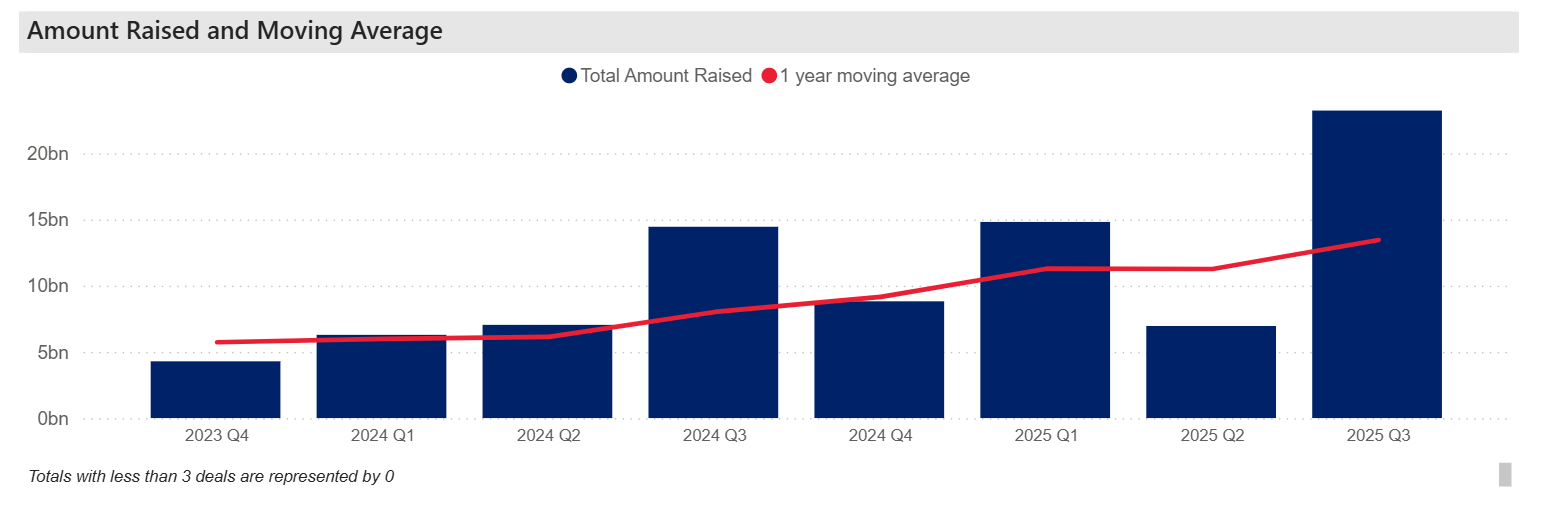

According to Cooley’s Q3 2025 Venture Financing Report, late-stage capital rebounded sharply despite lower overall deal volumes. Cooley handled 217 reported venture financings in Q3 2025, representing USD $23 billion in invested capital, signalling that capital is still flowing, but into fewer, higher conviction companies1.

Investment pools tightened, then stabilised

By 2024, venture funding in Southeast Asia had clearly shifted from volume to quality. In Singapore, government-backed initiatives helped maintain financial system stability, but startups were still affected by global investment trends.

What changed by 2026 was not a return to easy money, but a clearer equilibrium:

- Investors became more comfortable deploying capital again, but with stricter expectations

- Growth at all costs gave way to sustainable unit economics

- Cash efficiency and governance moved from ‘nice-to-have’ to ‘non-negotiable’

Investment outlook for 2026 and beyond

In 2026, the VC market in Singapore has moved from volume-led to quality-led, requiring founders to prioritise unit economics over top-line growth. Investors today are more willing to invest through cycles, provided founders demonstrate control, clarity, and resilience.

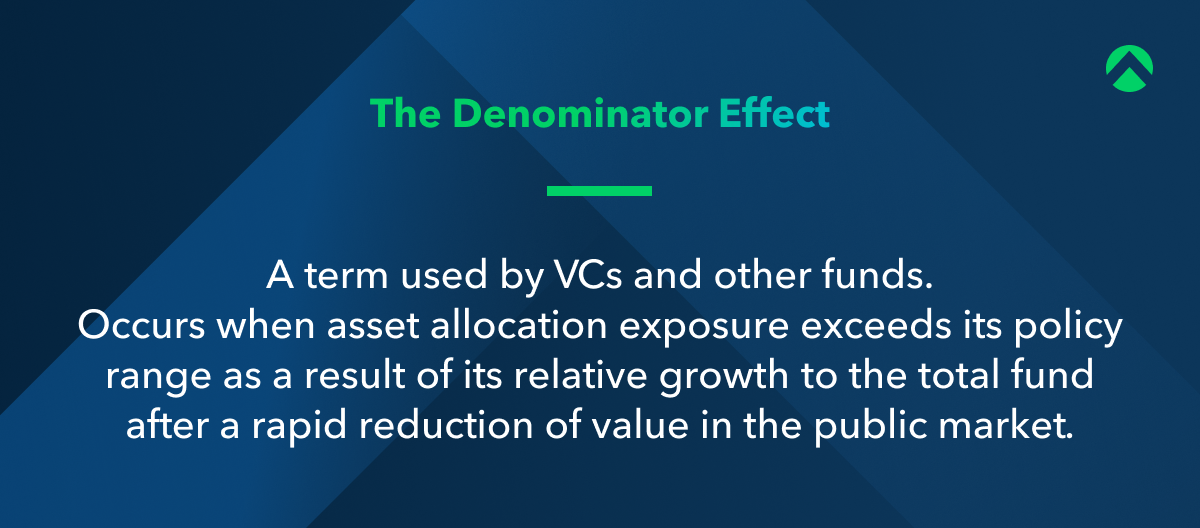

Many established venture funds spent the last few years managing the ‘denominator effect’, where public market corrections distorted portfolio allocations. As a result, deployment slowed. By 2026, allocations have stabilised, but cheque sizes remain measured.

In Singapore, new capital has increasingly come from:

- Family offices

- Corporate venture arms

- Regional funds with sector-specific mandates

- Select sovereign and institutional investors focused on long-term value

For founders, the takeaway is simple. Fundraising success in 2026 is a function of preparation and operational transparency, not market timing.

What this means for founders and CFOs in Singapore

Founders and finance leaders now need to focus on two core priorities:

Operational efficiency

Demonstrating control over cash flow, burn rate, and runway is essential. Investors now expect clear forward visibility into 24–36 months of runway, along with an explanation of how each dollar spent supports growth.

Investor readiness

A well-structured data room is no longer optional. Clear financial reporting, transparent metrics, compliance readiness, and documented governance processes are increasingly decisive factors in investment decisions.

Companies that show steady revenue traction, strong margins, and disciplined financial processes continue to attract interest even in cautious markets. However, investors are also more assertive when negotiating terms, making it critical for founders to review term sheets with a long-term lens.

Priorities when reviewing investor term sheets

Securing a good deal starts well before conversations with investors. It begins with clarity on what matters most to your business.

Before receiving term sheets

Set realistic valuations

Valuations in 2026 are grounded in fundamentals. Understanding pre-money and post-money mechanics, dilution scenarios, and future round signalling helps founders avoid misalignment later.

Define non-negotiables early

Not all terms carry equal weight. Some are flexible. Others can materially limit future fundraising or decision-making. Knowing your deal breakers in advance ensures you negotiate from a position of confidence, not urgency.

Watch for red flags

Beyond valuation, certain clauses deserve extra scrutiny. Restrictions on future funding, aggressive liquidation preferences, excessive control rights, or unusual veto powers can create long-term friction. These terms are difficult to unwind once agreed upon. Here is a quick list of some terms to be wary of and why:

Reviewing term sheets in a 2026 market

Higher valuations are not always better

A premium valuation may reduce short-term dilution, but it also raises performance expectations. With down rounds still representing nearly 20% of all deals, overly aggressive pricing can backfire in future rounds.

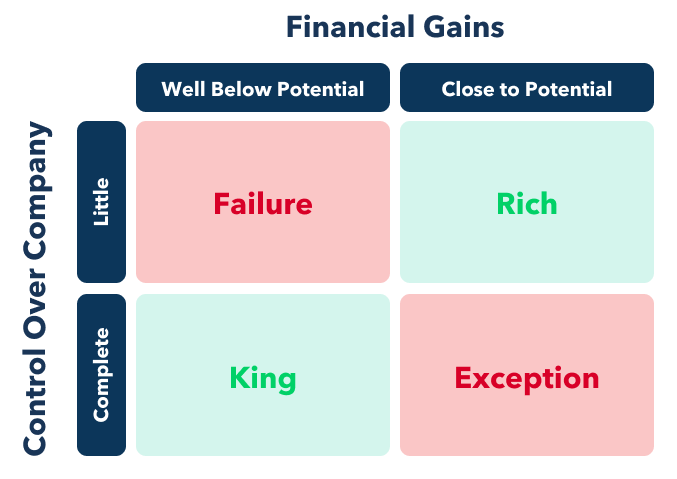

Rich vs King - How much control do you want

Successful CEO-cum-founders are an extremely rare breed, but that doesn't stop people from aspiring to be more. Every would-be entrepreneur strives to be a Bezos, Gates, or Zuckerberg, but few understand how difficult that can be. A majority of founders surrender management control by the 4th year, often replaced by a board-selected CEO who takes up a president or other board advisory role.

Founders must ask how much equity they are willing to part with to secure investment. Do they want to maintain control over all business decisions or cede that control to someone potentially more qualified? Is leading worth more than securing financial gain, or is it better to concede some control in exchange for financial flexibility? Founders’ choices are straightforward: Do they want to be rich or king? Few have been both.

Conclusion

Data from Cooley’s Q3 2025 report reinforces a clear message that capital is available, but concentrated. Investors are prioritising fewer companies, larger cheques, and stronger governance.

Singapore founders and CFOs who operate capital-efficient businesses, maintain long runways, and approach fundraising with preparation and realism are best positioned to succeed. A fair and well-structured term sheet signals alignment, not just capital.

Navigating this environment thoughtfully is no longer optional. It is a defining leadership capability for modern founders.

Frequently Asked Questions

- Cooley Go - https://www.cooleygo.com/data/

.webp)