Fast, low-cost international money transfers from Singapore

Trusted by 50,000+ modern businesses

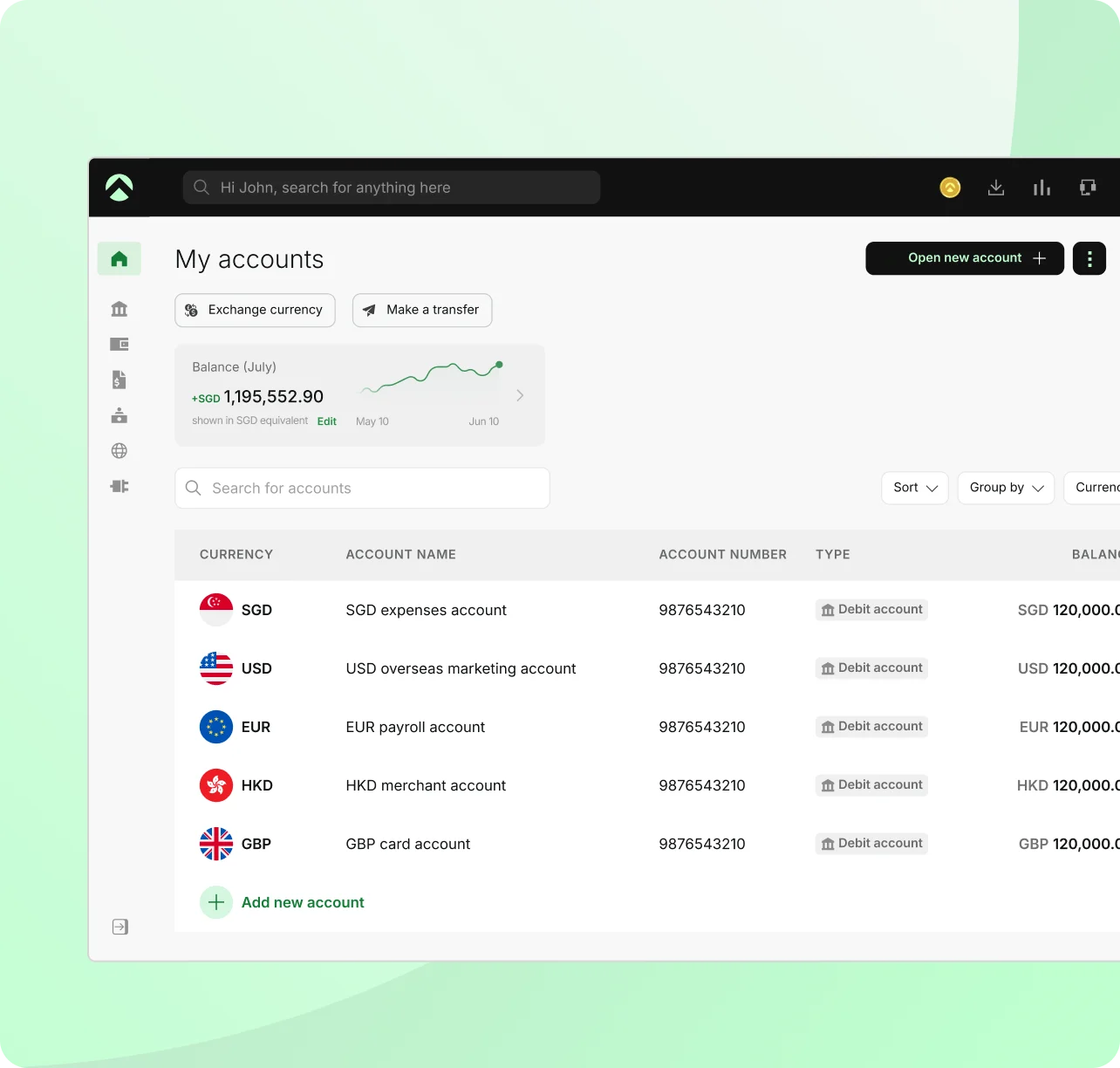

Powering your international payments

Enjoy real business savings on international payments

What you see is what you pay

Make fast international transfers

How Aspire compares for international business payments

Issue unlimited virtual cards to your team instantly

- Save more with FX pricing that beats most providers in the market today

- Send and receive international payments in 30+ currencies across 130+ countries at one of the best FX rates

- No hidden, account opening or monthly maintenance fees

Free local transfers for smooth transactions

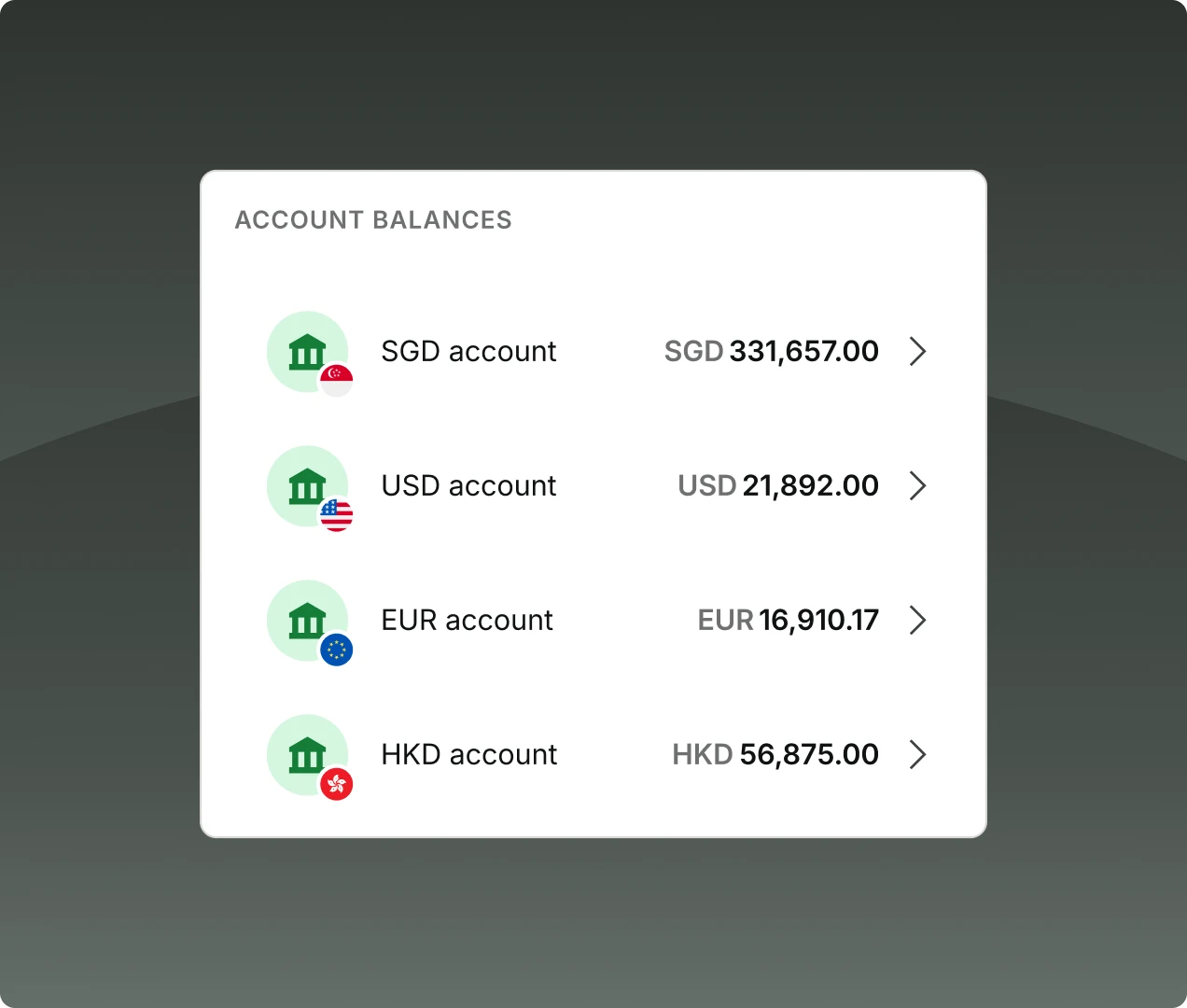

- Open local collection accounts in SGD, USD, EUR, GBP at no cost.

- Send, hold and receive funds in major currencies to transact with overseas suppliers and customers easily.

- Enjoy free local transfers in major currencies while enjoying market leading FX rates

Same day global payments & international transfers

- Safely send same-day local transfers and FX payments to 30+ major currencies directly from the Aspire App

- Fast reliable global payments to ensure your partners are always paid on time and improve cash flow

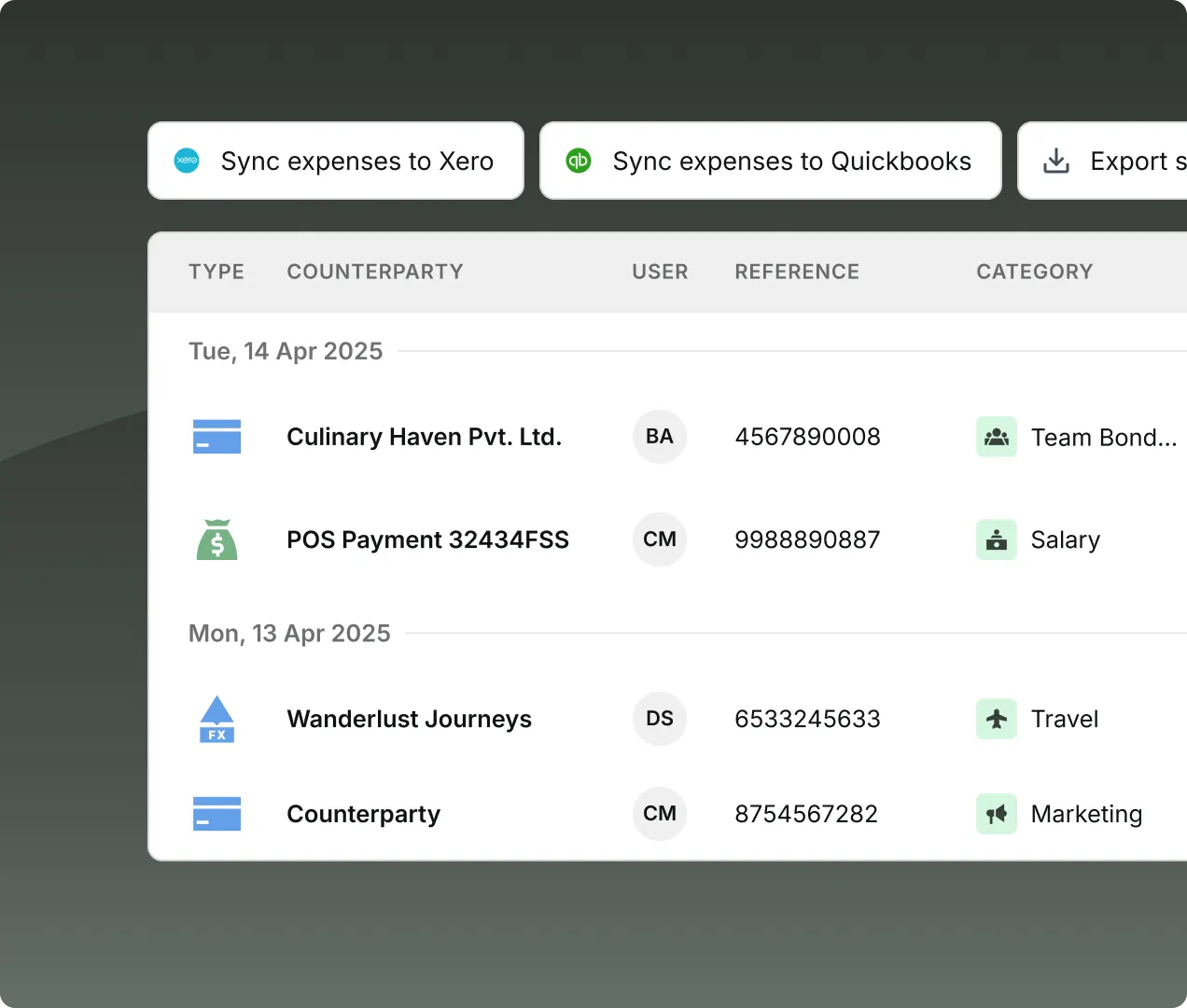

Sync transactions with your accounting software

- Close your books twice as fast, with all transactions synced with major accounting software

- Automate your accounting processes and improve your tracking accuracy

Hear it first from our customers

“As a startup, we needed more flexible solutions to support our increasing needs, as well as ones that’d make the most financial sense in supporting our growth.”

.webp)

Make global payments without breaking the bank

.webp)

FAQs about global payments & international money transfers

SWIFT is an abbreviation for the Society for Worldwide Interbank Financial Telecommunication and stands for a worldwide network of banks that work collaboratively to provide their customers with international bank transfers.

All SWIFT transfers are carried out via the payer's bank, which gets debited and routed through multiple intermediary banks before the recipient's bank is credited. This whole process can take up to 1-5 business days.

A local transfer uses a network of financial institutions to send money directly to a recipient’s local bank account. These transfers are settled in the local currency by the recipient’s bank. All you need are the recipient’s local bank account details.

Local transfers are generally cheaper and faster than SWIFT transfers. They typically settle instantly or within 1 business day, depending on the country’s payment infrastructure. By contrast, international wire transfers (via SWIFT) are used for cross-border payments but can take 1–5 business days and incur higher fees due to intermediary banks and currency conversion.

The key difference between international wire transfers and local bank transfers is that local transfers are typically faster and more cost-effective, while international wire transfers tend to involve higher fees due to intermediary banks and currency conversions.

Global payment is the process of transferring money to a bank account that is set up in a foreign country. This payment could be made to your supplier, your vendor, an employee, a business affiliate or any other entity. Making global payments involved strenuous processes and numerous fees in the past, however, the process is easier and more cost-effective today.

Generally, a global payment provider is involved, which functions as an intermediary between the payer & the receiver from different nations. They may collect funds locally and settle them in the recipient’s country using local payment networks, which reduces costs and processing times.

A global payment moves money to a bank account set up in another country, whether you're paying a supplier, vendor, employee, or business partner. Usually a global payment provider sits between you and the recipient, collecting funds locally and settling them in the recipient's country over local payment networks, which keeps costs and processing times down. With Aspire, you can send same-day transfers to over 30 currencies directly from the app.

Local transfers are the faster route. They send money directly to the recipient's local bank account and typically settle instantly or within one business day, while international wire transfers over SWIFT route through multiple intermediary banks and can take one to five business days. With Aspire, you can make same-day transfers to more than 30 major currencies, with free local transfers in major currencies and FX rates from just 0.22% above mid-market.

Start your journey with Aspire

Open your free account