What Is a SWIFT Code?

SWIFT codes, also referred to as Bank Identifier Codes or BICs are unique alphanumeric codes assigned to banks and financial institutions worldwide. SWIFT, an acronym for the Society for Worldwide Interbank Financial Telecommunications, develops and maintains these codes. They serve the important purpose of enabling secure and standardised communication between institutions during international financial transactions.

What’s the Purpose of a SWIFT Code?

The primary purpose of a SWIFT code is to ensure a smooth and reliable transfer of funds by accurately identifying the sending and receiving banks involved in a transaction. By utilising SWIFT codes, financial institutions can communicate securely and efficiently, reducing the risk of errors and delays in international transfers.

In essence, SWIFT codes act as the universal language that connects banks across borders, streamlining the process of international financial transactions and promoting a seamless global financial network.

What Does the SWIFT Code Look Like?

The SWIFT code consists of a combination of letters and numbers and follows a specific format. This code helps identify the branch, bank, and country of the account you're sending money to. It provides essential information about the account holder, transaction details, and geographical location.

Here's some interesting information highlighting the significance of SWIFT codes in the global financial system. During the year-to-date period of December 2022, Swift witnessed an average daily volume of 44.8 million financial messages exchanged through their network. This represents an increase of 6.6% over the same period a year ago.

The Structure of a SWIFT code

A SWIFT code follows a well-defined format composed of 8 to 11 characters. Let's break its components down from left to right:

- Bank Code: The initial four letters are dedicated to the bank's unique identifier, distinguishing it from other financial institutions.

- Country Code: The following two letters indicate the country where the bank is situated. This code adheres to ISO 3166-1 with 2 alphabetic country code standards.

- Location Code: The following two characters can represent the precise location of the bank branch. This portion may comprise letters, digits, or a mix of both.

- Branch Code: Concluding the SWIFT code are three additional optional characters that specify a branch within the bank. This segment proves valuable when a financial institution operates multiple branches in the exact location.

Here's what it looks like:

So, let’s look at an example of a SWIFT code for a bank in Singapore:

Bank: DBS Bank Ltd

SWIFT code: DBSSSGSG

Here, "DBSS" represents the bank code for DBS Bank Ltd, "SG" indicates the country code for Singapore, and "SG" at the end signifies the branch code or location code. The SWIFT codes for specific banks or financial institutions may differ, so it is always recommended to check with the bank itself.

Who Owns the SWIFT System?

SWIFT is actually owned by its members, which are certain financial institutions from around the world. These institutions represent different companies, so the ownership structure is quite diverse. SWIFT is overseen by the G-10 of Belgium, Canada, France, Germany, Italy, Japan, the Netherlands, Sweden, Switzerland, the United Kingdom, and the United States to ensure proper governance. Belgium is the lead supervisor, working with the US Federal Reserve.

Due to the vital role SWIFT plays in enabling secure communication among countries, every nation has a compelling reason to foster a positive relationship with this remarkable organisation. This cooperative approach ensures that SWIFT remains neutral and focused on providing secure and efficient financial communication services to its users worldwide.

How Does a SWIFT Transaction Work?

Your business may require you to send money internationally or receive it using SWIFT payment. Understanding the process is critical, whether it is sending funds to support your global operations, making international payments to suppliers or even receiving funds from international clients.

Here's how it works:

Step 1: Obtain the Necessary Information

To initiate a SWIFT transaction, gather the following details:

- Recipient's bank name, address, and country

- Complete legal name, current address, and account number of the recipient

- SWIFT code of the recipient's bank account

- Your Government-issued ID, like Unique Entity Number (UEN) or National Registration Identity Card (NRIC), for verification purposes

- Purpose of sending funds to the recipient

- Check for any more documentation or information required by your bank

Step 2: Initiate the SWIFT Transaction

Now that you have all the required information follow these steps:

- Access your bank's online platform to request an international wire transfer.

- Familiarise yourself with the associated fees and limits that may apply to sending funds abroad.

- Provide your bank with the recipient's country, desired currency, and other requested information.

- Initiate the transfer of funds using the SWIFT system, and keep a transaction record.

If you expect to receive funds, you must provide the sender with your bank's SWIFT number.

What Kind of Businesses Use SWIFT Codes?

If your business engages in international transactions and prefers using traditional bank services for sending and receiving payments, you may encounter situations where the bank requests a SWIFT code.

Below are examples of business entities that frequently use SWIFT codes:

- Goods & Service Providers: If you're a business that exports goods or provides services overseas, you will likely encounter SWIFT codes frequently. These codes help facilitate smooth and timely payments from abroad, ensuring you receive funds securely and without hiccups.

- Importers: When you purchase imported goods or services from other countries, using a SWIFT code adds an extra layer of assurance.

How to Find Your SWIFT Code?

You can typically find the SWIFT code of your bank or financial institution in your bank statements. You can also use certain websites to find your bank's SWIFT code. Contacting your bank or visiting your bank's website can aid you in finding the correct SWIFT code for your transaction.

You have numerous other options to find a SWIFT code. We have covered different methods for finding SWIFT codes here.

How Does SWIFT Payment Empower Banks for International Transactions?

Here’s how:

- Identification and Security: When banks use SWIFT codes, they can verify the parties' authenticity in the transaction. Since these codes provide essential details like the bank's name, country, city, and branch, which are crucial for successful transaction processing, this builds trust and ensures security.

- Simplified Communication: SWIFT codes provide a common language for banks to communicate efficiently and accurately. This makes conducting wire transfers, payments, and other financial activities easier, reducing the chances of errors or misunderstandings.

- Accurate Routing: SWIFT codes contain specific details about the recipient's bank, ensuring your money reaches the right destination. Despite the complex network of banks involved in international transfers, SWIFT codes help navigate the process smoothly.

- Compliance and Safety: Banks must comply with anti-money laundering (AML) and Know Your Customer (KYC) rules for international transactions. SWIFT codes assist banks in verifying the legitimacy of transactions, ensuring compliance with regulations and maintaining the integrity of the global financial system.

- Additional Services: SWIFT codes enable banks to offer various services, including correspondent banking relationships and international trade financing. They facilitate smooth interactions between financial institutions, supporting global economic activities and promoting international business transactions.

- Reduce Error or Delays: Using SWIFT codes, banks can securely and efficiently communicate transaction-related information, reducing the risk of errors or delays. This standardised system enhances transparency, minimises manual intervention, and helps banks comply with regulatory requirements for cross-border transactions.

How Does SWIFT Generate Revenue?

SWIFT operates on a membership model, and here's how they make money:

- Membership Fees: SWIFT members are classified into different classes based on their share ownership. When banks join SWIFT, they pay a one-time joining fee. Additionally, annual support charges vary depending on the member class.

- Message Charges: SWIFT charges users for each message sent through their network. The fees are based on the type and length of the message. Banks are charged based on their usage volume, and different charge tiers exist for banks with varying message volumes.

- Additional Services: Apart from its core messaging services, SWIFT offers additional services like business intelligence, reference data, and compliance services. These services provide valuable information and solutions to member banks, generating additional income for SWIFT.

However, it’s important to note that businesses are not charged for using SWIFT codes directly. Businesses may indirectly incur transaction fees or charges from their own banks for utilising SWIFT services, but they are not directly charged for the use of SWIFT codes themselves.

What’s the Relationship Between SWIFT Code & BIC Code?

Bank Identifier Codes or BIC code is a unique identifier for businesses. On the other hand, the SWIFT code is a specific type of BIC code assigned by SWIFT, the organisation responsible for managing the code system. Although technically, they are not the same, in practical terms, they can be used interchangeably.

So, if you are asked to provide your business's BIC code, they request the eleven-character code SWIFT assigned. The SWIFT code essentially serves as the BIC code assigned by SWIFT and signifies that the bank is part of the SWIFT network.

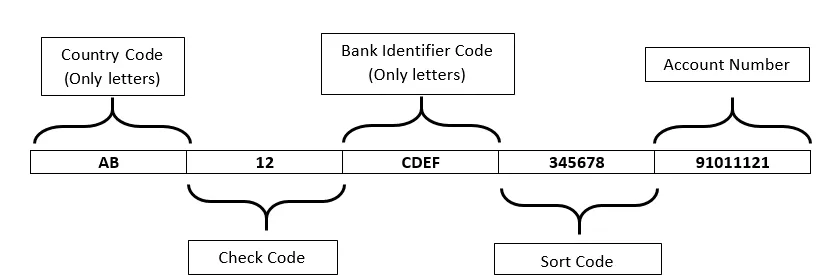

What’s the Difference between SWIFT codes and IBAN?

While a SWIFT code is used to identify a specific bank, your IBAN is used to identify your individual bank account for international transfers. The IBAN, an acronym for International Bank Account Number, is a standardised numeric system explicitly created for identifying overseas bank accounts.

Unlike a bank SWIFT code, which determines the bank, the IBAN goes further and identifies the specific bank account you're using.

Here’s what an IBAN code looks like:

Here, the initial two characters indicate the country code, consisting of letters. The following two characters indicate the numeric check digits. The remaining characters represent a lengthy and comprehensive bank account number.

An IBAN's primary significance lies in its ability to provide additional information for identifying international payments, particularly wire transfers. The bank may request you to provide both an IBAN and SWIFT code to ensure accurate identification of the destination for your money transfer.

However, some countries do not support the IBAN system universally. You'll just need the bank's SWIFT code to transfer money overseas to a country without IBAN. Rest assured, the SWIFT code will effectively guide the bank in routing your funds to the correct destination, even in countries where the IBAN system is not in place.

You may encounter other codes used for specific countries or regions.

For example, there is the Routing Transit Number (RTN) or ABA Number in the United States. This nine-digit code is used to identify domestic banks for transactions like electronic funds transfers, direct deposits, and checks.

In India, there is the IFSC code, an alphanumeric code designed for domestic bank transactions. It helps identify specific bank branches for secure transfers.

Whereas a sort code is utilised within the British banking industry to facilitate domestic money transfers between banks, this code identifies both the bank and the specific branch where the account is located.

Similarly, in Australia, there is the BSB Number. This six-digit code is used to identify banks and branches for domestic transactions within the country.

These codes serve specific purposes within their respective countries and help ensure domestic transactions' smooth and accurate processing.

Make global payments & transfers without breaking the bank with Aspire

Unlock the power of global payments and international transfers with Aspire. Experience the convenience of making transactions across borders at great FX fees.

Among Aspire's most notable features is our multi-currency account, which lets you manage multiple currencies. This flexibility empowers you to easily navigate international markets, avoiding unnecessary conversion fees and complexities.

In addition, we offer corporate cards that are designed to complement your global financial needs. These cards provide easy access to your funds, enabling you to purchase and withdraw cash in different currencies worldwide.

Transact globally more effectively and efficiently by breaking free from the limitations of traditional banking. Don't let excessive fees limit your business expansion across borders. Instead, take advantage of a financial solution that empowers you to do so.

.webp)