.png)

What are transaction fees?

Transaction fees are the money you pay card issuers and processors to process your customer's e-payments. This happens because several parties —banks and card processors —are involved in processing a single payment, and they charge a fee to make the transaction. It's generally 0.5-5% of the overall payment plus a fixed fee.

Suppose you hire a real estate agent to look for a house. The agent makes the transactions between you, the buyer, and the house owner, the seller.

He's the middleman who charges a fee to fulfill your requirement. Similarly, banks and card processors are a medium through which a payment is processed, so they charge money for their work.

How do per-transaction fees work?

With the rise of digital payments, your business can't survive relying on only cash payments. You must offer various payment methods such as debit cards, credit cards and e-wallets.

These payment methods are convenient for the customer but almost always come with per-transaction costs. Suppose a customer uses a UOB issued American Express card, and you have an arrangement with HSBC to get a payment terminal.

Here, three parties are involved in the payment:

- UOB, the issuer

- Visa, the card network

- HSBC, the acquirer

They will all take a share out of your total payment. HSBC, your acquirer, will process the payment. You pay a fixed fee to the acquirer and the network every time a payment is processed. The rate of this transaction fee is outlined in the merchant discount rate. It ranges from 1-3% of the overall transaction.

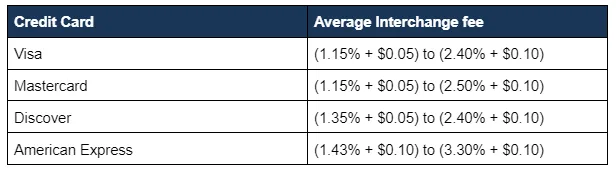

Visa and other networks likeMastercard, American Express, or Discover essentially charge the same credit card transaction fees as shown below:

You can't pass this fee on to the customer directly, but you can increase the overall costs to cover the transaction fee. This is why some businesses set spending limits in their stores to use e-payments. For example, a customer must spend a certain amount or above —say $80 —to use his cards or e-wallet. Customers with payments below the limit have to pay with cash.

Three factors affect overall transaction charges:

Interchange Rate

The interchange rate is applied to all credit and debit card transactions. Banks charge this fee to cover the handling costs and any transaction risks. Interchange fee makes up the most significant part of the transaction charges for your business as it includes a percentage fee plus a fixed fee.

Merchant Account Provider Fee

Your business must link its credit card to a merchant account. It allows you to process e-payments and deposit the money in your bank account. A merchant account is necessary as it doesn't wait for the customer to pay their credit card bills and deposit money into your account immediately after they make the payment.

In exchange, the merchant account provider charges a fee on top of the interchange fee. It involves a monthly statement fee, maintenance fee, and fall-below fee, which varies with the transaction volume and the type of your business.

The way the payment is processed

A customer can pay by swiping a card, over the phone, or via an e-wallet. Each mode of payment follows a different processing fee. It depends on how much risk is involved. For instance, a transaction where the customer pays with his card upfront is less risky than an unknown person paying online with a coupon.

Different types of transaction fees:

Interchange Fee

The interchange fee is the chief component of your overall transaction fee. Banks charge interchange fees to process your payments. It's the total of a percentage fee and a fixed fee.

For instance, to process a payment of $100, you'll have to pay a processing fee of 1.65% + 10 cents. The interchange rates vary with card companies and the payment methods, such as swiping the card, typing into a terminal, or online payment.

Terminal Fees

Retailers often use point-of-sale systems, which are a group of software designed to accept payments. The companies that provide these terminals charge a fee which is called a terminal fee.

Tiered Fees

In the tiered model, a payment processor divides the interchange cost into three categories, depending on the risk associated with it. The more the risk, the higher the processing fee.

The categories are as follows:

- Qualified rate: The transactions that meet all of the processor's requirements come under the qualified tier. For example, a face-to-face payment by swiping a card at a physical terminal is considered the lowest risk and, thus, comes with low fees.

- Mid-qualified rate: These are the transactions that don't meet specific requirements—for example, a transaction made by a mobile where the actual credit card was unavailable. The payment processor would charge higher for this payment as high risk is involved.

- Non-qualified rate: Payments like e-commerce, reward cards, or signature cards fall into this category as neither the card nor the cardholder is present for payment. These are charged the highest fees.

Subscription Fee

Some card providers allow a subscription plan rather than charging per transaction. It gives you a pre-set idea of how much you will pay for transaction charges. Subscription plans are easy to incorporate and are charged monthly or annually.

Foreign transaction fees

If you're doing business outside Singapore, banks apply extra charges, called foreign transaction fees, on your credit card. They also depend on the card issuer and card processor's policies.

Foreign transaction fees are applied when:

- you make an online transaction abroad

- pay a foreign vendor in your home country who completes the transaction in his local currency

- withdraw money from ATM in a foreign country

You can save foreign transaction fees by:

- Checking the terms and conditions of various credit card companies and choose the one with the least transaction fees. Some cards also offer zero foreign transaction costs. If you don't already have it, apply for them to save money on international transactions.

- Opening a local bank account if you have repeated transactions with the same business partner or retailer overseas.

- Opening a multi-currency business account to send and receive payments in 30+ currencies with great exchange fees. Companies like Aspire takes care of your invoicing and integrates it with your accounting system so you can focus on business by converting every single payment into your local currency.

Acquirer fee

An acquiring bank is registered with card networks. It accepts credit card payments from the merchant on the network's behalf.

Balance Transfer Fee

If you owe your credit card company some money and can't pay the higher interest, you can transfer that whole debt to a new credit card with a lower interest rate. The new credit card company clears your debt with the older one.

This transfer allows you to pay the same debt to a new company for lower interest. But the catch is that the new company will charge a balance transfer fee so you can move over your debt.

Calculate which amount is more - the previous debt with the given interest rate or the new debt with lower interest plus the balance transfer fee. If the shift is profitable, transfer your debt to the new company in exchange for the balance transfer fee.

Other Types of fees

Other than the types mentioned above, the service provider can charge more credit card transaction fees depending on your activity, such as:

- Checking account fee

- Overdraft fee

- Maintenance fee

- Statement fee

- Termination fee

How to calculate the transaction fee?

Transaction fees are not uniform for all transactions. It depends on your card and account providers' policies. There are various factors in play, such as

- Risk in the transaction

- Type of card used

- Pricing set by the payment processors

Two main criteria involved in transaction fees are:

- Flat fee: Your account provider charges a fixed fee of around 20-50 cents per transaction.

- Percentage Fee: Your account provider retains a small percentage - around 3% - of your total transactional value.

Here's an example of processing rates from Elavon, shown on Costco’s website

Let's assume a customer uses a Visa debit card issued by Citibank to pay $100 to your business. We'll understand how the transaction fee is divided among all involved parties and what the merchant gets.

You, as a merchant, must have a contract with an acquirer outlining the set payment processing rates. So, the payment of $100 goes straight to the acquirer, and they debit their fees upfront, which is 1.99% + 25 cents.

- Transaction Value: $100

- Acquirer’s take (1.99% + 25 cents): $2.24

- Merchant's share: $97.76

The acquirer must now distribute this money amongst Visa, the issuer, and itself. So, how does each get paid? Let's look at the issuer's perspective.

The issuer is also entitled to interchange fees. The amount depends on the payment method and the risk involved in the transaction. For convenience's sake, we'll assume this was a low-risk transaction. So the issuer is entitled to $1.65% + 15 cents, which is called the interchange fees.

- Transaction Value: $100

- Issuer’s take ($1.65% + 15 cents): $1.80 (Interchange Fees)

The issuer must distribute the remaining $98.20 among the merchant, Visa company, and the acquirer. We already know that the merchant got $97.76 after debiting the merchant discount fee. So, the remaining 44 cents will be distributed between Visa and the acquirer.

Now, Visa's fee is 0.11%, depending on the risk involved but since we've assumed a low-risk situation, let's go with 0.11%

- Transaction Value: $100

- Visa’s take (0.11%): 11 cents

- Remaining money: $98.09

Again, we know the merchant gets $97.76, so the acquirer's take is 33 cents.

- Consumer pays: $100

- The issuer receives: $1.80

- Visa receives: $0.11

- Acquirer receives: $0.33

- Merchant receives: $100 - $2.24 (overall fees)= $97.76

How to save on transaction fees?

Transaction fees are an unavoidable charge. But there are ways to reduce it. Try the tips below to save up on your transaction fees:

Apply either a surcharge or convenience fee

The best way to save transaction fees is to pass them on to the customers. There are two ways to do it:

- A convenience fee is applied when your customer makes a credit card payment online. It's not applied if the customer swipes the card on the counter.

- A surcharge applies on all credit card transactions, irrespective of how they're made. You must abide by the state laws on both fees.

Remember to check the state laws about both convenience and surcharge fees.

Encourage customers to swipe cards

Risk is an essential factor in determining your overall transaction fee. So, encourage your customers to swipe cards for over-the-counter transactions as they're safer and invite less interchange fees.

Ask your processor

Consult with your payment processor about the transaction fee. They know minute details of your fee schedule and can offer you a workaround for your transaction fee. A friendly phone call can get you creative ways to save money or rate reduction for your loyalty.

Use Aspire's Visa Card for international payments.

Aspire's multi-currency business account lets you save a lot on international card transactions with a nominal fee on foreign transactions, compared to other corporate cards.

On top of this, we offer 1% cashback on all qualified SaaS and digital marketing spending. With Aspire, you scale and save together.

Save more with Aspire.

The transaction fee is an unavoidable expense. You can't stop online transactions to save your business from it. But you can choose options that dilute its effect on your business.

Aspire's a multi-currency business account and the Visa card comes with two-time lesser FX rates than banks. It comes with the added convenience of accounting integration, so you save time spent on bookkeeping.

Are you thinking of marketing your business online? Aspire also offers 1% cashback on SaaS and marketing spending. It can't be better than this. Become an Aspire partner today and save time and money together.

.webp)