What is accounting?

Accounting is the systematic collection, processing, and reporting of a company’s key financial information. It’s how your business organises and keeps track of all financial transactions to make them understandable for shareholders, stakeholders, and other relevant company members.

Some of the most common accounting procedures and activities include identifying transactions, analysing financial data, receipt tracking, auditing financial statements, payroll accounting and tax collection.

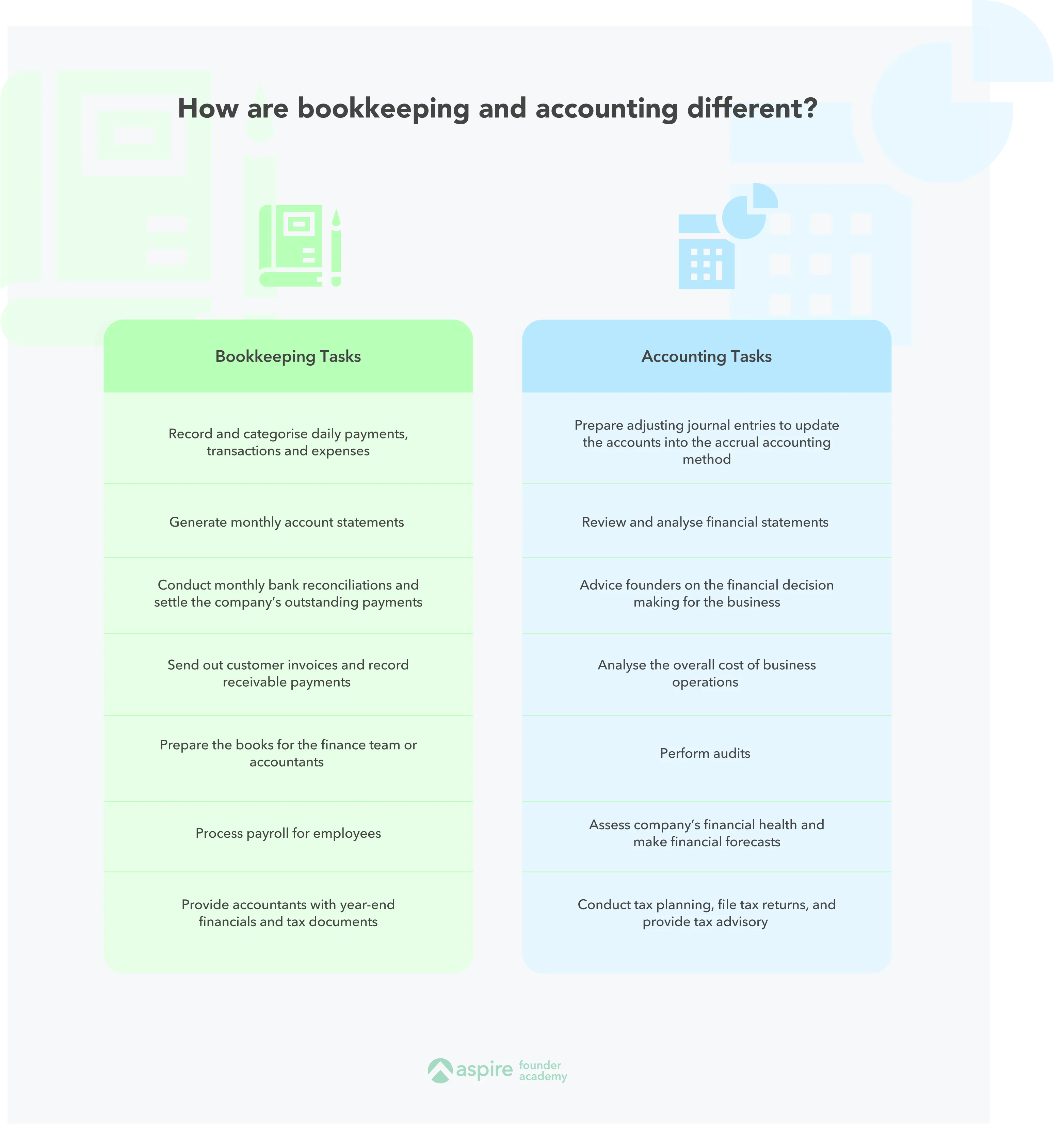

What is the difference between bookkeeping and accounting?

Most business owners think that bookkeeping and accounting are the same. While they have similarities in the context of business, they still vary greatly.

Bookkeeping is a more administrative task, mainly concerned with recording a business’s financial transactions and activities. The bookkeeper’s role is to ensure this information is accurate and up-to-date.

Accounting is the ‘application’. With the information from the bookkeeping process, accountants gain valuable insights into the company’s financial health, facilitating financial forecasting and a better understanding of your business finances.

These are some of the key differences between accounting and bookkeeping.

Why accounting matters for start-ups

It’s nearly impossible to run a business without having your finances in order.

With the key quantitative data derived from these accounting practices, founders can track cash flow, provide investors with accurate financial information, and gain perspective on their financial position as a start-up.

Here are just some out of the many ways accounting can benefit businesses like yours:

- It’s an effective way to measure profitability.

- It allows business owners to create financial forecasts.

- It helps finance teams gain valuable insights about spending.

- It keeps your financial records organised.

How to streamline your accounting

1. Choose your business entity

Your business structure or entity determines how your liability and the taxes you’ll pay.

For instance, sole proprietors in Singapore have unlimited liability as they are not considered separate legal entities. But for Limited Liability Companies (LLCs) in the country, the personal assets of business owners are protected from being liable for the company’s debts.

Here’s a quick look at the different business structures in Singapore, according to ACRA:

- Sole Proprietorship or Partnership

- Limited Partnership (LP)

- Limited Liability Partnership (LLP)

- Company or Corporation

2. Open a business account

Opening a business account is a priority for all business owners at the beginning of their start-up journey. Separating personal expenses from business finances allows for more organised business records, accurate tax and deductions, and access to credit solutions.

On top of that, this gives you an added touch of credibility and professionalism.

Pro-tip: Looking for a business account designed especially for start-up founders and modern entrepreneurs? Check out the Aspire Business Account today.

3. Determine your accounting system and method

Business entity, check. Business account, check. Now what?

The final step to streamlining your business is choosing the right accounting method. You’ve got two options: the accrual or cash-basis accounting method. Find the system that works best for you and your business, and make sure to stick with it.

These are the differences between cash-basis and accrual accounting:

- Cash-basis Accounting: One of the easiest accounting methods because it only records revenue when cash is received, and expenses are paid.

Since this system does not record accounts receivable and payable, business owners and finance teams can immediately know how much resources they have at their disposal.

- Accrual Accounting: With this method, transactions are only entered into the books when the invoice is generated instead of when the cash has been received. Common examples include ‘sales on credit’ or ‘purchase on credit’.

Pro-Tip: Already using accounting software for your business? Sync with your Aspire Business Account in just a few clicks.

In-house or outsourced accounting: which is better for my business?

One of the key questions you’ll have to ask yourself as you grow your business is if you should outsource your accounting, hire an in-house accountant, or even do it all on your own. Finding the right person to manage your finances is one of the most integral parts of running a start-up, especially in the earlier stages.

Let’s explore the options.

Handling your accounting on your own

If you’re a small business owner, chances are you’d want to handle your business’s books on your own to save some extra cash. There are plenty of free resources online to help you out—from financial statement templates to informational videos on how to get started with all your accounting duties.

On top of that, managing your own finances gives you firsthand insights into your business’s performance, making you more skilled at monitoring your financial records.

Outsourcing your accounting

If your start-up has a steady foundation and some extra cash, it makes sense to outsource accounting services.

You’re likely to have less time for all sorts of bookkeeping activities. Hiring an external person will take away some of the heavy lifting, allowing you to focus on crucial operational tasks that demand more time and attention.

Hiring an in-house accountant

Finally, if your business is growing and ready for an in-house team, hiring an additional team member to your finance team is the way to go. One of the greatest benefits of hiring an in-house accountant is the sheer availability that outsourcing lacks.

From conducting market analysis to removing a plethora of tax worries, in-house accountants will know the ins and outs of your company's financials, adding a greater sense of loyalty for both employer and employee. Onboarding an additional member means extra work for your HR team, however.

No matter what you choose, remember to take the time to determine your bandwidth and resources as a business owner.

Pro-Tip: Good news for foreign directors! Gain access to an all-inclusive accounting package when you incorporate your start-up with Aspire Kickstart.

Basic accounting terms every business owner should know

To get you up to speed on all the jargon there is to know, here are some introductory accounting terms that you’ll definitely come across in your day-to-day activities as a founder.

Cash Flow: The total amount of money that comes in and out of a company due to various business activities.

(Working) Capital: The initial amount of money business owners have to spend or invest in growing their business. These funds are typically liquid and accessible at any time and don't include assets or liabilities.

Assets: A company’s tangible or intangible resources with economic value, which are responsible for generating cash flow and improving sales for the business. These include cash, property, operational equipment, trademarks, patents and copyrights.

Liabilities: Everything your business owes, including loans, taxes, credit card balance, mortgages, accounts payable and accrued expenses.

Accounts Receivable: The balance money due to a business for the provision of goods or services, which will be recorded as an asset on your company’s balance sheet.

Accounts Payable: The exact opposite of accounts receivable. Accounts payable is the money a company owes its vendors and supplier, which are considered short-term liabilities. These include logistics, transportation, licensing and equipment.

Income Statement: A financial document that shows you the income and expenditures of a company, also known as a Profit & Loss (P&L) statement.

Expenses: The operational costs of conducting business in order to generate revenue.

Profit and Loss Statement: A statement used to summarise a company’s financial positions and overall performance by assessing the revenues, expenses and costs.

Equity or Shareholder’s Equity: The amount of money that would be returned to key shareholders once a company pays off all its debts and sells its assets.

Retained Earnings: An accumulated portion of a company’s profits or net income left after a business has paid out dividends to its shareholders at the end of a reporting period.

Fiscal Year: Also known as a financial year, this is an important one-year accounting period companies use to calculate annual financial statements.

Burn Rate: The rate at which a company is spending its start-up capital before generating any form of positive cash flow or profit.

Profit Margin: The percentage of total revenue that remains after deducting all costs, taxes and other administrative expenses

Essential records you need to keep track of

Now you’re familiar with some of the basic accounting terms, let’s get acquainted with some important financial records.

Whether you’re outsourcing to an accountant or hiring an in-house professional to manage all your bookkeeping tasks, it’s useful for founders to familiarise themselves with this information.

- Payroll: All documentation about paying employees, such as their pay rate, direct deposit authorisation forms and tax deductions.

- Invoices: A payment request that documents the transaction between a buyer and seller, which is critical for internal audits and controls. Most common for suppliers, vendors, freelancers and contractors.

- Bank Statements: A printed record showing the summary of financial transactions of a specific individual or business. This tool helps account holders monitor their finances and identify errors, if any.

- Financial Statements: Unlike bank statements, which the bank typically sends, financial statements are generated and prepared by the company’s management. This provides shareholders with a general overview of the company’s financial health, position and performance.

- Corporate Card Statements: Similar to bank statements, a corporate card statement will provide you with a summary of how your company credit card has been used over a specific billing period.

- Start-up Costs: All expenses incurred during the entire process of business planning, research and development, and the actual business launch fall under start-up costs. This includes everything from marketing and promotion, market research, employee training, utilities, equipment and permits.

- Proof of Payment: Especially for e-commerce businesses or companies that regularly deal with product shipments from overseas, transaction proof is an essential document you’ll need in the accounting process. In a dispute between the seller and buyer, this is written proof that the related purchase has been paid for.

- Bills: As a business owner, you want to build good credit with your vendors by paying your bills on time. In the context of accounting and finance, bills can be filed under accounts payable.

Pro-Tip: Process your bills automatically with Aspire Bill Pay. Simply pay by forwarding an email, and we’ll take care of the rest.

Why taxing matters when it comes to accounting

Business owners often think tax and accounting are two separate entities. But they are more intertwined than you might think. Accounting processes, such as calculating financial statements, are used to make tax calculations and payments.

Like in any other country, businesses pay corporate taxes in Singapore—from IRAS tax to sales tax. Singapore is a tax haven for many foreign investors and business owners, with the lowest corporate tax rate (17%) in Southeast Asia.

The role of an accountant or the finance team during tax seasons is to prepare tax returns, assess financial statements to ensure accuracy, and help companies meet the necessary tax compliance requirements and regulations.

The three core financial reports for start-ups

The general purpose of financial statements is to provide vital information to shareholders, creditors and investors on a company’s overall financial position.

In the field of accounting, every company’s annual report has three essential financial reports: A balance sheet, income statement and cash flow statement.

.webp)

1. Balance Sheets

Also known as the statement of financial position, a balance sheet is the most important financial document in any business, regardless of size and valuation. The balance sheet records a company’s financial position by showing the assets the business controls, the liabilities that it owes, and the amount of equity that belongs to the relevant equity holders.

The balance sheet formula: Liabilities + Equity

2. Income Statements

Income statements help us understand whether the operations of a firm created economic profit or loss. They also enable us to identify key trends such as revenue growth and gross profit.

The income statement formula: Net income = Revenue - Expenses

3. Cash Flow Statements

A cash flow statement shows us the movement of cash created by a business’s operations and activities. While an income statement reveals whether or not a business made a profit, a cash flow statement focuses on the amount of cash generated throughout an accounting period.

This statement can be categorised into three categories of activities:

- Operating Activities: From the accounts receivable to the cash from inventory, operating activities are vital in funding a company’s day to day operations.

- Investing activities: As a business grows, start-ups may choose to purchase long-term assets such as real estate and other businesses as investment securities, which can enhance the cash flow of a company.

- Financing Activities: All cash flow between a business and its owners or creditors can be referred to as financing activities. With activities such as selling stock and paying cash dividends, this financial record focuses on how a business raises capital and repays its investors.

Knowing your numbers is essential to growing your business

Prioritising finance and accounting is key to a successful business. You may think that it’s just numbers, but these figures help you make well-informed and calculated financial decisions.

.webp)