.webp)

What Does GST Mean For a Singapore Company?

If you are a GST registered company, the primary implication is that you will have to collect GST from customers for the products and services you provide. You will then have to pay this to the IRAS while filing GST returns.

Let’s assume that you sell a product worth S$1,000 to a customer. If you are a GST registered company, you have to issue a GST invoice which also contains the GST amount. This invoice, including the GST amount and the GST registration number, is called the tax invoice.

In Singapore, the GST rate is 7%. So, for a tax invoice for a product costing S$1,000, you will have to issue it inclusive of GST of S$70. The total GST invoice amount will come up to S$1,070.

Every quarter, you must pay the total GST collected to the IRAS. You can follow the IRAS GST guide to understand how to file GST and make GST payments.

Charging and Accounting for GST as a GST registered Company

If you have a GST registration number, i.e., you are a GST registered company, you will need to charge your customers GST at a rate of 7%. This amount will be included in your tax invoice.

However, you only need to charge and account for GST if you deal in standard-rated supplies. Standard-rated supplies are all goods and services that are made in Singapore. It excludes exported goods, international services and exempt supplies.

If you make relevant supplies such as local sales of mobile phones, memory cards or off-the-shelf software exceeding S$10,000, they will be subject to customer accounting and you will need to provide a customer accounting invoice. In such instances, you don’t have to charge GST to your GST registered customer. Your GST registered customer will have to account for this GST as their output tax instead. To be eligible for customer accounting, the customer must be a GST-registered business.

A customer accounting invoice is similar to a tax invoice. However, it contain the following details in addition to the tax invoice details:

- The GST registration number of the customer

- A statement or disclaimer clarifying to your customer that customer accounting has been used and they have to account for GST when filing their returns

In the event that you sell both prescribed and non-prescribed goods and services, you will need to apply the principles of customer accounting only to prescribed goods and services. In addition, the sale value must exceed S$10,000.

Regardless of whether you employ customer accounting methods or not, you will have to report the supply in your GST returns.

Filing GST Returns

If you have GST registration from IRAS, you are responsible for ensuring that GST returns are filed correctly and on time.

All GST returns have to be filed via the MyTax portal. You will have to file GST returns within a month from the end of each accounting period. You still need to file a ‘NIL’ GST return if you have no GST transaction. If you are filing GST voluntarily, you will be on the GIRO plan for GST payment. GIRO deductions are made on the 15th day of the month after payment is due. For instance, if your GST returns are due on December 31, 2022, then you must make the payment by January 15, 2023.

What Happens If You File GST Late?

If you pass the deadline for filing GST, then the IRAS will impose a late submission penalty of S$200 immediately after the time of IRAS GST filing has lapsed. An additional S$200 will be imposed as a penalty for every month that the amount is outstanding. The maximum penalty that the IRAS can impose for late submission is S$10,000.

The IRAS may also take additional action, such as appointing agents to recover GST, issuing a Travel Restriction Order that prohibits you or other company members from leaving Singapore or take legal action.

What If You Don’t File GST?

As a GST registered company, it is compulsory for you to file GST, even if you have no GST transactions during the accounting period. If you fail to pay GST, it will be considered a punishable offence. The IRAS can levy fines of up to S$10,000 and even imprisonment of up to six months.

Initially, the IRAS will issue a notice and charge the penalty fee. Upon repeated default of payment, the IRAS may summon you to court. If you have received a court notice and do not wish to continue with the legal proceedings, you must do the following at least a week before the court hearing:

- File all the outstanding GST returns

- Pay the compensation amount

If you need more time to make the payments for some reason, you need to go to court on the date of the hearing with a letter of authorization from your appointed agent, appealing for postponement.

If you fail to attend court, there may be further legal actions against your business, including a warrant to arrest you, your partner, company director or anyone else in charge.

Maintaining Proper Business and Accounting Records

As a GST registered business, you must keep all business and accounting records for at least five years. Even if you have wrapped up the company or deregistered from GST, you will still need to keep these records handy for the time in case the IRAS summons for the same.

Types of Records to Keep

You must maintain various records, including tax invoices, income, purchase and business expense records, statements and accounting schedules, etc. You can make this a part of your accountant responsibilities to ensure that they are maintained according to the required standards.

- Income Records

All your income records must be maintained using tax invoices or simplified tax invoices. You must save the receipts issued or cash register tapes from every sales transaction that has taken place. If you have rental income, you need a rental agreement signed by both the tenant and you. Any documents relevant to income, such as credit notes for returned goods, export-related records, or evidence of payment received, must be maintained.

- Purchase and Business Expense Records

As with income, all purchases and business expenses must be supported with the proper documentation proof. Purchase invoices and receipts have to be maintained. All documents related to imports of goods or services, payment vouchers, rental agreements for rent paid, bank statements to corroborate any cash payments, etc., must be kept as proof.

- Other Documents to Support GST Declarations

In addition to income and expense proofs, any documents that affect the output tax and input tax as reported in your GST return must also be kept handy. This could include details of using any business asset for personal reasons, selling business assets, moving goods from customs-licensed warehouses, etc.

- Statements And Accounting Schedules

Your accountant’s responsibilities should include maintaining and keeping track of all your records, including bank statements of your business, stock lists, general ledgers that explain your assets and liabilities and revenue and expenses, financial statements including Balance Sheet, Profit and Loss Statement, Cashflow Statement, sale and purchase listings in the required format, etc.

- Account of GST Filings

You must also maintain a record of your total input and output tax for each accounting period. This will ensure that you file your GST returns accurately and produce documentation in case the IRAS asks for proof.

- Electronic Records

You can maintain all your records in electronic format. However, you must follow certain guidelines to maintain the same.

What To Do If You Lose Some Records?

In case you misplace any of the records in the five-year tenure, there is a possibility that your input tax claim will be rejected.

If you lose supporting documents to prove the export of goods or providing international services, you will be required to pay standard-rate supply GST on the goods or services.

The IRAS may also levy penalties for failing to maintain the documents to support your GST declaration.

GST Pricing

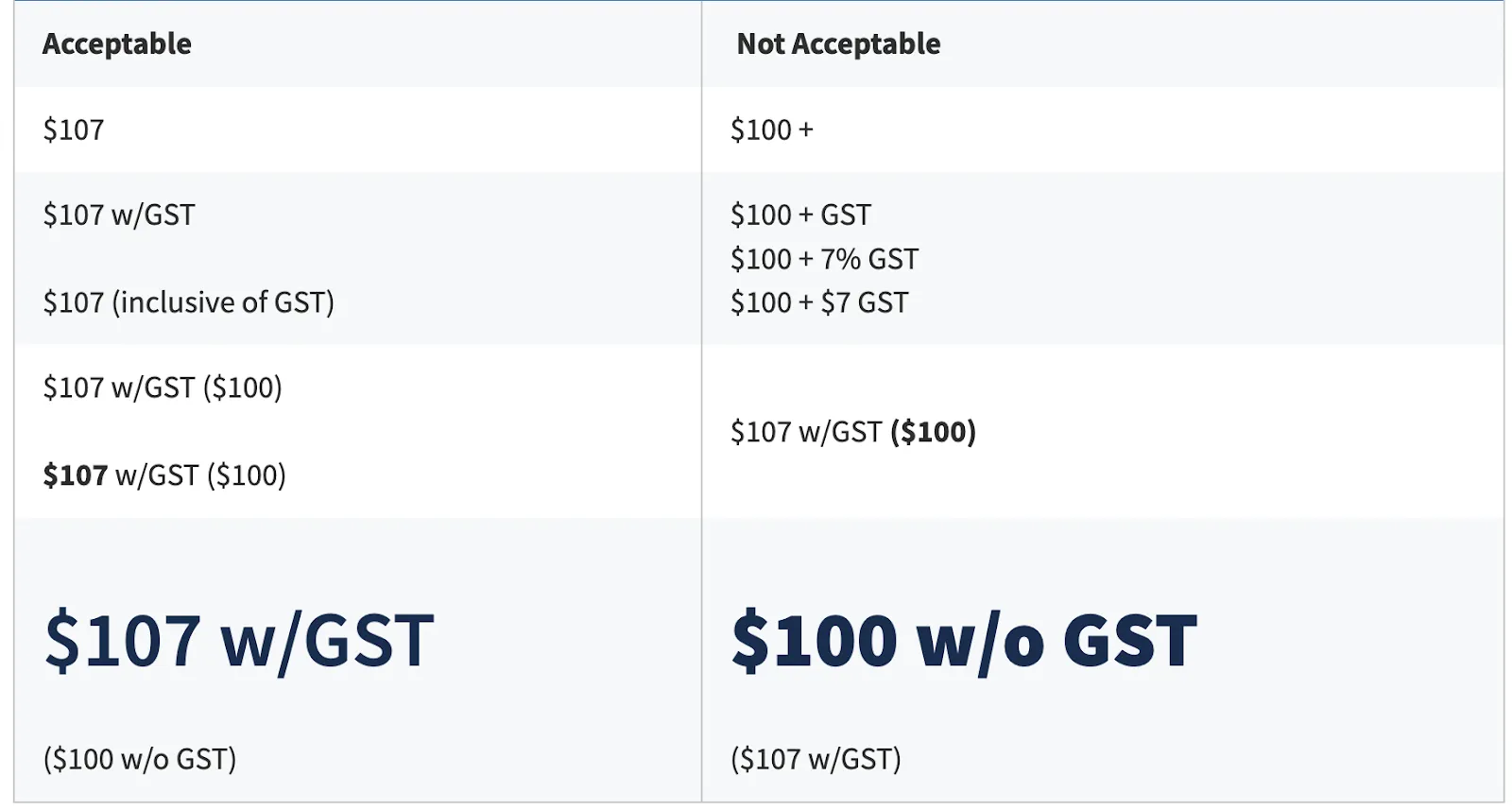

As a GST registered business, all your pricing should be inclusive of GST. Whether on price displays, advertisements, publications or quotations made to the public regarding the sale of goods or services, they must always include the GST-inclusive pricing.

If you want to display the GST-exclusive price as well, you can do so, but the GST-inclusive pricing must be displayed at least as prominently as the non-GST pricing. It is not enough to provide a disclaimer that the prices shown are exclusive of GST.

Take a look at this example of acceptable and unacceptable price displays:

However, if you are a hospitality or food and beverage business charging service tax, you do not need to display GST-inclusive price lists. This is because it becomes operationally difficult to display GST-inclusive prices because of the additional component of the service charge. However, you must still provide a disclaimer saying prices are subject to GST and service charges.

Tax Invoices with GST Registration Number

As a GST registered business, you must issue tax invoices for all your standard-rated supplies. You can issue a simplified tax invoice if your total payable amount, including GST, does not exceed S$1,000. No matter what kind of tax invoice you issue, it should always carry your GST registration number.

Obligations for Compulsory GST-Registrants

In case you are registered to pay GST compulsorily, you must comply with all the responsibilities of a GST-registered company as outlined in the article above. Here’s a quick summary of the things you must do:

- Charge GST for standard-rated supplies

- Issue a tax invoice or a customer accounting invoice, as applicable

- File GST returns on time and accurately

- Maintain all relevant business and accounting records

- Display prices with GST

The Comptroller is authorized to cancel your business’s compulsory GST registration if there is reasonable evidence that you are committing or involved in fraudulent activities.

Obligations for Voluntary Registrants

If you have registered for GST voluntarily, then you must:

- Make use of the GIRO plan for payment and refund of GST

- Be GST registered for at least two years after GST registration

- Fulfil all the responsibilities of a GST registered business

- Start making taxable supplies within two years of GST registration

- Follow any other compliances as issued by the IRAS

If you do not meet these requirements, the Comptroller may cancel your voluntary GST registration.

How to Deal With Any Business Changes as a GST registered Company?

Along with all the obligations mentioned above, as a GST registered company, you must also notify the Comptroller of any business-related changes. The changes have to be notified within 30 days.

Some of the changes that you need to notify the Comptroller of include:

- Any alteration in the GST mailing address

- A change in the business constitution or ownership

- Any change in the partners or details of the partners

- A change in the partnership agreement, even with the existing partners

What To Do If You Deregister Your Business From GST?

If you deregister yourself from paying GST, whether you were previously a compulsory or a voluntary GST registered business, there are certain protocols you must follow. After your GST registration is cancelled, you must still account for GST on business-related assets held on the last day of registration if:

- GST was previously claimed on the business assets

- The total market value of these business assets is more than $10,000

The assets could include inventories, fixed assets, non-residential properties and goods imported under the various GST schemes.

Let’s understand this better with an example. Say that you have claimed input tax in the past on plant and machinery of S$50,000 and a land used for business purposes costing S$500,000. On the last day of your GST registration, the open market value of the plant and equipment is S$55,000 and the land is S$600,000. While filing GST F8, you have to account for output tax on S$655,000, which will amount to S$45,850 (7% of S$655,000).

Conclusion

Whether you are a compulsory registrant or a voluntary registrant for GST, you will need to fulfil obligations required by a GST-registered company. This includes filing your GST on time, raising tax invoices, employing customer accounting wherever applicable, etc. If you fail to meet any of the required obligations, you will be subject to consequences from the IRAS. Before you go in for GST registration IRAS, go through the IRAS GST Guide to understand your responsibilities so that you can fulfil them effectively.

Download this article as an e-book: Responsibilities Of A GST Registered Company In Singapore

.webp)