.webp)

What is withholding tax in Singapore?

When a non-resident company or individual receives payment from a Singaporean company or individual for goods or services provided in Singapore, a percentage of that income must be paid as tax to the Inland Revenue Authority of Singapore (IRAS). The IRAS does not collect this tax from the non-resident company after it has received the payment. Instead, the Singaporean company making the payment is required to withhold a percentage of the payment amount and remit this amount to the IRAS. This explains why this tax is called a withholding tax. Singapore’s withholding tax is, therefore, an advance payment on the recipient’s tax liability.

This withholding tax does not apply to Singapore-resident companies and individuals. Furthermore, the withholding tax rate in Singapore may be lowered under the country’s numerous tax treaties.

What is a non-resident company or individual?

A company is considered a tax resident of Singapore if its control and management remains in the country. The IRAS defines control and management as “the making of decisions on strategic matters, such as those concerning the company’s policy and strategy”. One way of determining if a company fulfils this tax residency condition is if its board of directors meets and takes strategic decisions in Singapore. A company’s Singapore residency status typically lasts for one year of assessment and can, therefore, change from year to year.

That explains what a Singapore-resident company is. But what is a non-resident company?

Applying the same IRAS rule, a non-resident company is one whose control and management lies outside Singapore. This could mean:

- Its board of directors do not meet in Singapore.

- It has no critical employees based in Singapore.

- Its local director in Singapore is a nominee.

- Its local director in Singapore takes no strategic decisions.

Whether a company is incorporated in Singapore or not has no bearing on its tax residency. As we mentioned in our previous blog, Singapore Corporate Tax Rate and System, incorporation is the legal process of setting up a company. Based on incorporation, a non-resident company in Singapore can be:

- A company incorporated in another country, including the Singapore branch of a foreign company.

- A company that is incorporated in Singapore but does not meet the tax residency requirements above mentioned.

Similarly, a non-resident individual is one who has been in Singapore for less than 183 days in the year when they provided goods or services to a Singapore entity. They include:

- Foreign professionals. This is a broad category including experts invited to Singapore by private organisations, government agencies, and statutory boards; speakers and academics who organise seminars and workshops in Singapore; trainers, coaches, and consultants; Queen’s counsels (legal experts); and individuals operating in Singapore through a foreign firm.

- Public entertainers, such as musicians, actors, sportspersons, and dancers.

- Board directors.

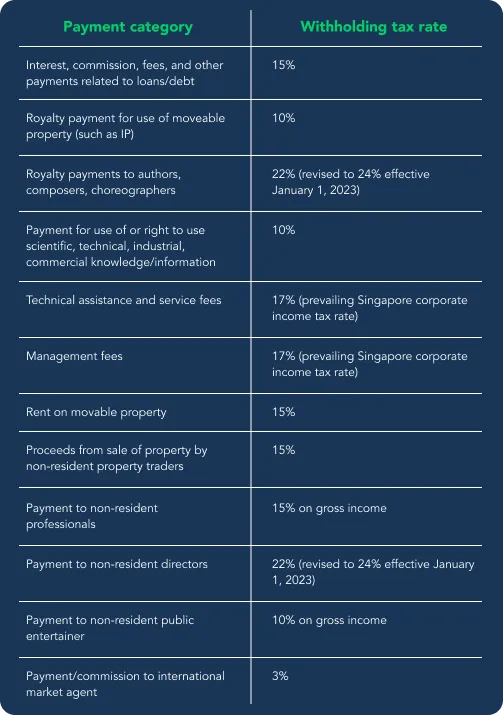

Singapore withholding tax – Eligible income sources and tax rates

The following categories of payments made to Singapore non-residents are subject to withholding tax at the mentioned rates:

- Interest, commissions, fees, and any other loan-related payments invite a 15% withholding tax.

- Royalty payments for the use of movable property (intellectual property, software, etc) or made to authors, composers, and choreographers are taxed at between 10% and 22%.

- Payments for the use of or the right to use scientific, technical, industrial, or commercial knowledge attract a 10% withholding tax.

- Technical assistance and service fees (for the application of scientific, technical, industrial, or commercial knowledge, for example) are taxed at Singapore’s prevailing corporate income tax rate of 17%.

- Management fees (for assistance in managing a business, trade, or profession) are also taxed at the corporate income tax rate of 17%.

- Rent and other payments for the use of movable property attract a withholding tax of 15%.

- Proceeds from the sale of property by non-resident property traders are subject to a 15% withholding tax.

- Payments to non-resident professionals are taxed at 15% of gross income. However, within this category, payments to non-resident directors attract a higher tax rate of 22%.

- Payments to non-resident public entertainers are taxed at 10%.

- Payments or commissions to international market agents (Casino Regulatory Authority of Singapore licence-holders authorised to make casino marketing arrangements) attract a 3% withholding tax.

Income sources exempt from withholding tax

Certain types of payments to non-residents are exempt from withholding tax in Singapore. These include:

- Dividends, or the distribution of profits to shareholders. The Singapore dividend withholding tax rate is 0%.

- Payments made for the charter of ships and leasing of containers for transport of goods by sea.

- Payments made by banks and finance companies for the running of their business.

- Payments of any kind (interest, royalties, commissions, etc) made to the Singapore branches of non-resident companies.

What is the Singapore withholding tax rate on different income sources?

Key facts about withholding tax in Singapore

The main points to remember about Singapore withholding tax:

- It applies only to certain types of payments made to non-resident entities.

- The payment must be made by a Singapore entity (company or individual).

- The Singapore-sourced payment must be for goods or services provided in Singapore.

- Singapore withholding tax rates differ according to the type of payment and range from 10% to 22%.

- Withholding tax rates might be lowered under Singapore’s tax treaties – better known as Avoidance of Double Taxation Agreements (DTAs) – with other countries.

Deadline to pay Singapore withholding tax

The withholding tax must be filed and paid by the 15th of the second month from the date of payment to the non-resident. For example, if the payment was made on August 20, 2022, then the withholding tax must be filed and paid by October 15, 2022.

How to determine date of tax payment

The date of payment is the earliest of the following:

- Payment due date as per the contract between the two trading companies

- Date of invoice, in case there is no contract

- Date on which payment is credited to the non-resident’s bank account or any account authorised by them

- Date of actual payment.

The conditions for determining date of payment differ slightly for remunerations to non-resident directors. Here, the date of payment is the earliest of the following:

- Date of general meeting when the paying company approves the non-resident director’s fees either in the form of arrears (for services already provided) or as advance (for services not yet rendered)

- Date on which payment is credited to the non-resident’s bank account or any account authorised by them

- Date of actual payment.

What if you miss the tax deadline?

In the event of failure to pay withholding tax, the IRAS may initiate the following actions:

- Impose a late payment penalty that is 5% of the total tax amount. If the tax remains unpaid 30 days after the due date, an additional 1% penalty per month is charged, up to a maximum of 15% of the total tax amount.

- The IRAS may also appoint a third party, such as the payer’s bank, as a tax recovery agent. This could lead to inconvenience in operating their bank account.

- Against defaulting sole proprietors and partners, the IRAS may issue a travel restriction order, preventing them from leaving Singapore until the tax is paid in full.

- Other legal actions include a penalty that is three times the tax amount, a fine of up to SGD 10,000, and up to three years in jail.

The IRAS may waive the late payment penalty under certain circumstances:

- If it is the tax payer’s first waiver appeal and they have filed and paid their withholding tax on time for the last two years.

- If they have paid the overdue tax in full.

- If they show initiative to pay their tax on time in future by signing up for GIRO (General Interbank Recurring Order) payment facility.

Keep in kind though that meeting any or all of the above conditions does not guarantee a penalty waiver, and that the IRAS will make a decision on a case-by-case basis.

How to file withholding tax in Singapore

Withholding tax must be filed electronically on the IRAS website on Form S45. However, if the taxpayer has multiple payment records that they wish to submit in bulk, they may opt for the Excel-based S45 Offline Data Entry (ODE) form. Important filing details to keep in mind include:

- Date of payment

- Total payment amount subject to withholding tax (converted into Singapore dollars if it is in a foreign currency)

- Period for which payment is made (if it is more than a year, separate filings must be made for each year)

- Period of engagement of the non-resident entity (if it is more than a year, separate filings must be made for each year)

- If the taxpayer is seeking relief under a tax treaty, they must check the relevant box during filing.

Once the form is successfully filed, an acknowledgement page will open up detailing how the withholding tax can be paid. After payment, the taxpayer may view and download the payment confirmation from the website.

Withholding tax can be paid via internet banking, telegraphic transfer, various other e-payment services, and on the GIRO platform.

The IRAS allows the correction of errors made during filing (such as entering the wrong date of payment). Simply go to the IRAS website, click on ‘View/Amend S45 Form’, and edit the form. Once submitted, the fresh form will replace the previous one.

Claiming relief on withholding tax under tax treaties

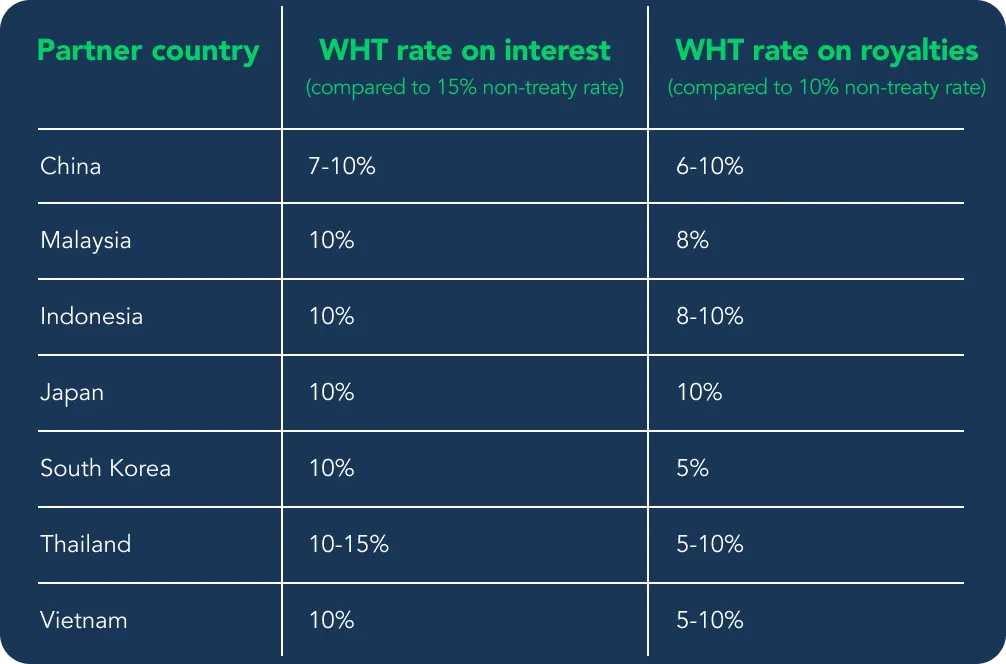

It is possible to reduce your Singapore withholding tax burden – through a reduced tax rate or exemption – under an Avoidance of Double Taxation Agreement (DTA). The purpose of such an agreement is to avoid double taxation in international trade – when the same income source is taxed in two different countries. Singapore has an extensive network of DTAs with multiple countries. Here’s how you can claim relief on your Singapore withholding tax under a DTA if the agreement has such a provision:

- On the withholding tax filing form, check the ‘Double Taxation Relief’ box and applicable tax rate. In the case of payments to non-resident professionals, the ‘Claim for Relief under Avoidance of Double Taxation Agreement’ box must be checked.

- Obtain documents from the non-resident entity proving that they are a resident of the DTA partner country and are, thus, eligible for tax relief. A Certificate of Residence is usually accepted.

- Scan and upload the documents to the IRAS website by the due date. If the claim is for the current year (2022, for example), then the documents must be submitted by March 31 of the following year (March 31, 2023). If the claim is for a preceding year, the documents must be submitted within three months of the withholding tax filing.

For an example of how tax relief under a DTA works, let’s take the tax treaty between Singapore and Indonesia. Under this agreement, withholding tax on royalty payments has been lowered from the prevailing 15% in Singapore and 20% in Indonesia. Instead, royalty payments for the use of or the right to use copyright of literary, artistic, or scientific work (radio or television films or tapes, etc), patents, trade marks, secret formulas or processes will be taxed at 10%. Similarly, royalty payments for the use of or the right to use industrial, commercial, or scientific equipment will be taxed at 8%. For more examples of withholding tax relief under DTAs, see the table below:

How DTAs can reduce Singapore withholding tax rates

The countries listed above are Singapore’s top trade partners with which it has a provision for withholding tax relief.

A full and deep understanding of the meaning of withholding tax and all it involves has numerous benefits for companies and individuals doing business in Singapore. It means a smoother tax filing experience, never missing out on fulfilling your tax compliances, and making the most of any Singapore tax deductions on offer.

.webp)