Definition of a smart card

A smart card is a physical card with a built-in memory chip. This memory chip allows it to transfer data electronically. Credit cards, work pass cards, smart health cards, SIM cards, and certain ID cards are all examples of smart cards. Smart cards can perform all their necessary functions and store all their data without connecting to any external databases, thanks to their integrated circuits.

This feature makes smart cards much more secure and flexible than magnetic stripe cards, which rely on external systems to work. Unlike traditional versions, smart cards can do much more. They are used for secure data storage, user authentication, and running applications, too.

Smart card market outlook: What 2026 looks like

Smart cards continue to grow steadily as digital payments, digital identity, and secure authentication expand globally.

Recent industry estimates show:

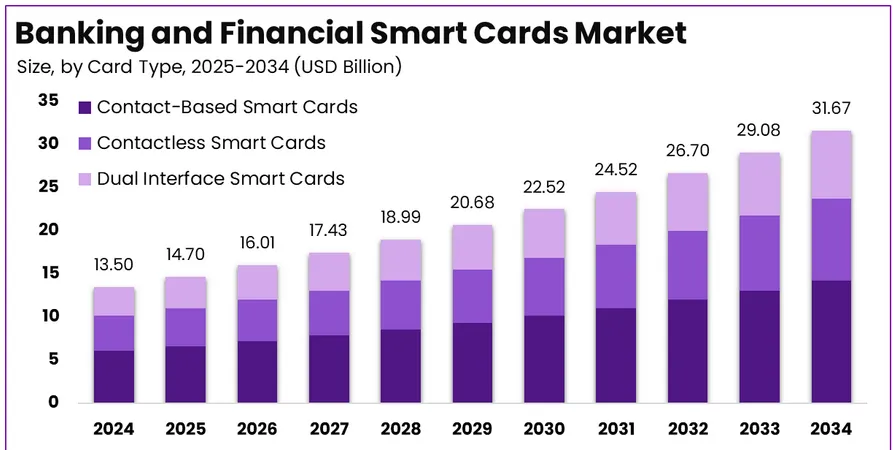

- The global smart card market is valued at roughly USD $12.4 billion in 20262, with long-term growth expected to nearly double by 2036.

- Other forecasts place the broader smart card ecosystem at around USD $17.5 billion in 2026, with continued strong growth through the next decade.

- Growth is driven by banking, telecom, transport, government digital ID, and secure enterprise access systems.

For business owners, this matters because smart cards are now deeply embedded in payment infrastructure, employee identity, and cybersecurity systems.

In many industries, they are becoming standard rather than optional.

Types of smart cards businesses use today

By the communication interface

- Contact smart cards: These must be inserted into a reader to complete a transaction. They are commonly used in secure banking, enterprise access, and government identity systems.

- Contactless smart cards: These use NFC or RFID technology and work by tapping the card near a terminal. They are widely used across Singapore's transport, retail, and fast payment environments.

- Dual interface smart cards: These support both insert and tap payments on the same chip. They are increasingly used in corporate and banking environments because they work across multiple use cases.

By processing power

- Microprocessor cards: These function like mini-computers with built-in processors. They support encryption, multiple applications, and dynamic data storage. They are commonly used for corporate cards and secure digital identity.

- Memory cards: These only store data and do not process it. They are typically used for prepaid cards, loyalty programs, and simple transit systems.

Emerging business applications

- NFC digital business cards: These allow professionals to tap their card on a phone to instantly share contact details or profiles.

- Biometric smart cards: These include fingerprint authentication on the card itself, adding an extra layer of security for transactions and access.

Applications of Smart Cards

Smart cards are now a go-to solution for secure payments and identity management across industries. With strong in-built security features, they help modern businesses simplify workflows while keeping sensitive information safe.

How corporate smart cards improve business payments and financial control

Smart cards help businesses move from manual, reactive expense tracking to real-time digital control. Instead of reviewing expenses after they occur, businesses can set spending rules before transactions happen. Beyond payments, smart cards also support expense management, improve cash flow visibility, and reduce fraud risk.

1. Enhanced control and compliance

Smart corporate cards allow businesses to set spending rules in advance. Businesses can assign budgets to teams or employees and restrict usage to approved merchant categories such as travel or software. Policy rules, such as daily limits or location restrictions, can be automatically enforced at the point of sale.

2. Operational efficiency and automation

Smart cards reduce manual expense reporting by recording transactions in real time. They integrate with accounting software such as QuickBooks, Xero, and NetSuite to automatically categorise expenses and match receipts. Issuing cards to employees also removes reimbursement delays.

3. Advanced security and fraud prevention

Smart cards use chip-based encryption that generates a unique code for every transaction. Businesses can also create virtual cards for specific vendors or subscriptions. Cards can be frozen instantly if suspicious activity is detected.

4. Financial and cash flow benefits

Many business cards offer payment cycles of 28 to 31 days, helping preserve working capital. Businesses can also earn cashback, rewards, or travel benefits on operational spending.

Limitations of Smart Cards to consider

While smart cards offer clear pros, there are a few cons to think about before fully committing to them:

- Cost: Smart cards and smart card readers are more expensive than traditional cards. Then there are the costs of technology upgrades, reader devices, and the cards to be considered.

- Compatibility: Not all smart cards are compatible with all smart card readers. Some, especially the patented ones, need specific reader-software combinations to work.

- Security Risks: Despite being the flagbearer of security, smart cards are not foolproof against cyber threats. Regular updates and security protocols are critical to protecting data and enhancing security.

- Durability: Even though smart cards are designed to be durable, they can still be damaged if not handled with care.

How Aspire's corporate cards simplify your business

Scaling a company requires precise expense management. This is where Aspire’s Corporate Card comes in. It transforms your expense management experience into a streamlined, secure, and transparent process, enabling you to focus more on business strategy and less on tedious manual work.

Built in collaboration with Visa and Nium and fully integrated with Aspire's Business Account, it helps you track expenses in real time, reducing manual work and end-of-month chaos. It is designed as a digital solution for the new generation of business owners who demand better banking experiences. Whether you're a startup scaling fast or a small team handling overseas suppliers, this card fits right in. You will get real-time alerts, advanced fraud protection, and global reach—wrapped in a clean, digital experience.

No more chasing team members for receipts. No more reconciling messy expense sheets. Gain real-time visibility over team spend. Aspire gives you the visibility and control you need to focus on what really matters: growing your business.

.webp)